Assessing Your Retirement Readiness: A Comprehensive Checklist for Your Golden Years

Picture this: you’re sipping your morning coffee on a Tuesday, and instead of rushing to catch the train to work, you’re leisurely planning your day around personal interests. Sounds dreamy, right? But here’s the reality check – that dream retirement doesn’t just happen overnight. It requires careful planning, honest assessment, and strategic decision-making that should ideally begin decades before you hand in your final resignation letter.

Whether you’re 25 and just starting your career or 55 with retirement on the horizon, assessing your retirement readiness isn’t just about crunching numbers in a spreadsheet. It’s about creating a roadmap to financial freedom and peace of mind. The truth is, many Americans are woefully unprepared for retirement, with studies showing that nearly half of all households have no retirement savings at all. Don’t let yourself become part of that statistic.

This comprehensive checklist will help you evaluate where you stand today and identify the gaps you need to fill before you can confidently step into your post-career life. Think of it as your retirement readiness GPS – it’ll show you exactly where you are and help you navigate to where you want to be.

Financial Foundation Assessment

Let’s start with the elephant in the room – money. Your financial foundation is the bedrock of a comfortable retirement, and it’s more complex than simply having a fat savings account. You need to evaluate multiple financial streams and safety nets that will support you when your regular paycheck stops coming in.

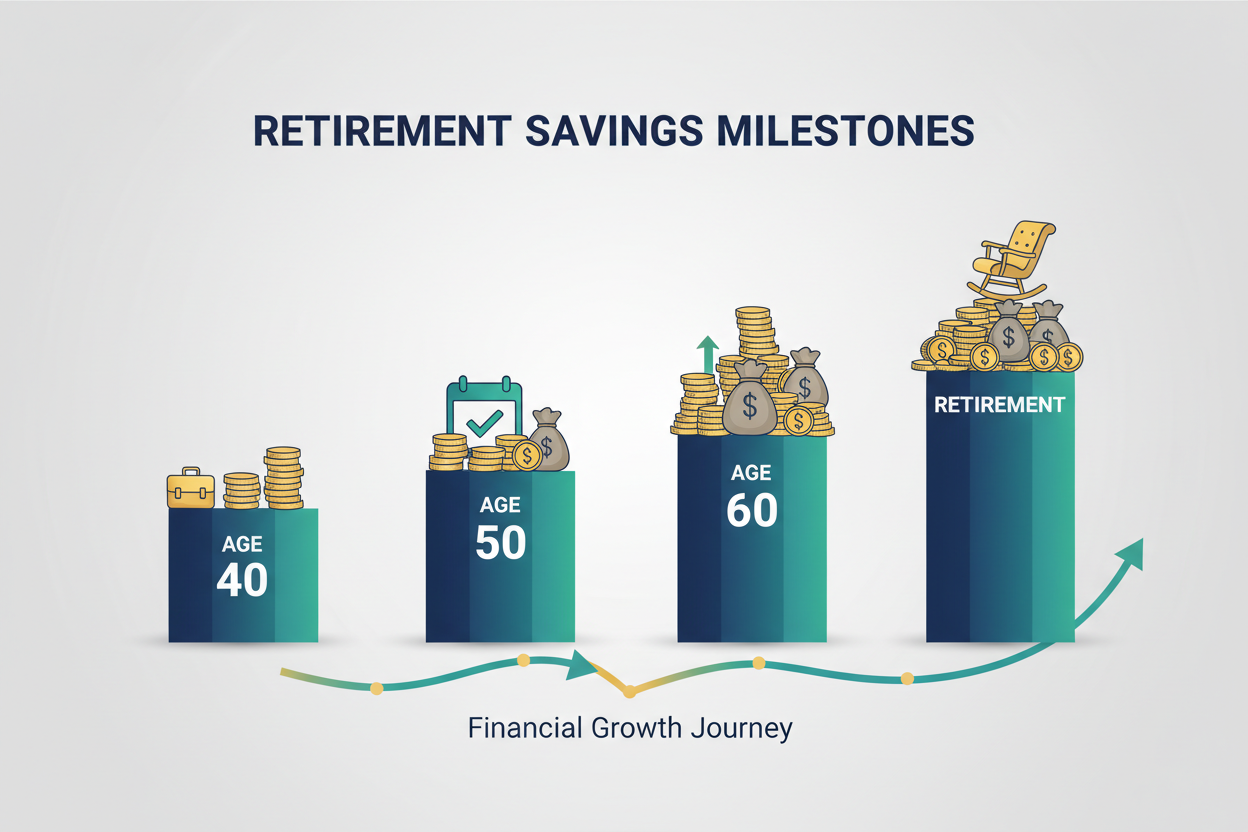

First, take a hard look at your retirement savings accounts. How much do you currently have in your 401(k), IRA, or other retirement vehicles? A good rule of thumb is to have saved at least 10 to 12 times your annual salary by the time you retire. If you’re 40 years old, you should ideally have three times your annual salary saved. At 50, it should be six times, and at 60, you’re aiming for eight times your annual income.

But don’t panic if you’re behind – the key is knowing where you stand so you can adjust your strategy accordingly. Maybe you need to increase your contribution percentage or take advantage of catch-up contributions if you’re over 50. Perhaps it’s time to reassess your investment allocation or consider working a few extra years to boost your nest egg.

Next, evaluate your debt situation. Ideally, you want to enter retirement debt-free, especially when it comes to high-interest credit card debt. Your mortgage is a different story – some financial experts argue that if you have a low-interest rate, you might be better off investing the money you’d use to pay it off early. However, there’s something to be said for the peace of mind that comes with owning your home outright.

Healthcare and Insurance Coverage

Healthcare costs in retirement can be a real budget buster, and unfortunately, Medicare doesn’t cover everything. The average couple retiring today will need approximately $300,000 to cover healthcare expenses throughout retirement – and that’s just for Medicare premiums, deductibles, and out-of-pocket costs for services that Medicare covers.

Start by understanding what Medicare does and doesn’t cover. Medicare Part A covers hospital stays, Part B covers doctor visits and outpatient care, Part C is Medicare Advantage (an alternative to Parts A and B), and Part D covers prescription drugs. You’ll likely need supplemental insurance to fill the gaps, which means additional monthly premiums to factor into your retirement budget.

Consider opening a Health Savings Account (HSA) if you’re eligible. HSAs offer triple tax benefits – contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. After age 65, you can withdraw funds for any purpose without penalty, though non-medical withdrawals will be taxed as ordinary income.

Don’t forget about long-term care insurance. The likelihood of needing some form of long-term care is higher than you might think – about 70% of people over 65 will need long-term care services at some point. Long-term care insurance can help protect your retirement savings from being depleted by nursing home or in-home care costs.

Social Security Benefits Optimization

Social Security will likely form a significant portion of your retirement income, so understanding how to maximize these benefits is crucial. The system is more complex than many people realize, and the decisions you make about when and how to claim benefits can have lasting financial implications.

Your full retirement age (FRA) depends on when you were born, ranging from 65 to 67. You can claim benefits as early as age 62, but doing so will permanently reduce your monthly payments. Conversely, if you delay claiming until age 70, you’ll receive delayed retirement credits that increase your benefit by about 8% per year.

For married couples, the claiming strategy becomes even more important. Spousal benefits, survivor benefits, and the timing of each spouse’s claim can significantly impact your household’s total Social Security income over your lifetimes. It’s often worth consulting with a financial advisor or using Social Security optimization software to explore different claiming scenarios.

Create an account at ssa.gov to access your Social Security Statement, which shows your complete earnings history and provides estimates of your future benefits. Review this annually to ensure your earnings are being recorded correctly, as errors could reduce your future benefits.

Retirement Lifestyle Planning

Money is just one piece of the retirement puzzle. You also need to think about how you want to spend your time, where you want to live, and what kind of lifestyle you envision for yourself. These decisions will directly impact your financial needs and overall happiness in retirement.

Start by estimating your retirement expenses. A common rule suggests you’ll need 70-80% of your pre-retirement income, but this varies widely depending on your circumstances. If you plan to travel extensively, pursue expensive hobbies, or relocate to a high-cost area, you might need 100% or more of your current income. Conversely, if you’ll have a paid-off mortgage and plan a simpler lifestyle, you might get by with less.

Consider where you want to live in retirement. Will you stay in your current home, downsize locally, or relocate to a different state? Each option has financial implications. Staying put might mean higher property taxes and maintenance costs but lower moving expenses. Downsizing could free up equity but might involve transaction costs. Moving to a different state could offer tax advantages or lower living costs but might separate you from family and familiar healthcare providers.

Think about how you’ll spend your time. Many retirees struggle with the loss of structure and purpose that work provided. Will you volunteer, pursue hobbies, start a small business, or work part-time? Having a plan for your time can contribute significantly to your happiness and mental health in retirement.

Estate Planning Essentials

Estate planning isn’t just for the wealthy – it’s essential for anyone who wants to ensure their wishes are carried out and their loved ones are protected. A comprehensive estate plan becomes even more important as you approach retirement and your assets grow.

At minimum, you need a will that specifies how you want your assets distributed after your death. Without a will, state law determines how your property is distributed, which might not align with your wishes. Your will should also name an executor who will be responsible for managing your estate.

Consider whether you need a trust. While not everyone needs a trust, they can be valuable tools for avoiding probate, minimizing taxes, and providing for beneficiaries who might not be ready to handle a large inheritance. Revocable living trusts are popular because they allow you to maintain control of your assets during your lifetime while providing for seamless transfer after death.

Don’t forget about beneficiary designations on your retirement accounts, life insurance policies, and other financial accounts. These designations typically override your will, so it’s important to keep them updated, especially after major life events like marriage, divorce, or the birth of children or grandchildren.

Advance directives are also crucial. A healthcare power of attorney designates someone to make medical decisions on your behalf if you’re unable to do so. A living will specifies your wishes regarding end-of-life care. A financial power of attorney allows someone to manage your financial affairs if you become incapacitated.

Income Replacement Strategies

Once you stop working, you’ll need to replace your employment income with retirement income. This typically comes from a combination of sources, often referred to as the “three-legged stool” of retirement: Social Security, employer-sponsored retirement plans, and personal savings.

Develop a withdrawal strategy for your retirement accounts. The traditional rule suggests withdrawing 4% of your portfolio in the first year of retirement, then adjusting that amount annually for inflation. However, this rule has limitations and might not be appropriate for everyone. Market conditions, your age at retirement, and your risk tolerance all factor into the optimal withdrawal rate.

Consider the tax implications of your withdrawals. Traditional 401(k) and IRA withdrawals are taxed as ordinary income, while Roth account withdrawals are generally tax-free. Having a mix of account types gives you flexibility to manage your tax liability in retirement. You might also consider Roth conversions in years when your income is lower to reduce future required minimum distributions.

Think about whether you’ll work in retirement. Many retirees today work part-time, either by choice or necessity. This can provide additional income, help your savings last longer, and offer social interaction and a sense of purpose. However, if you claim Social Security before your full retirement age, earned income above certain thresholds can reduce your benefits.

Professional Guidance and Resources

While self-assessment is valuable, retirement planning can be complex, and professional guidance can help you avoid costly mistakes and optimize your strategy. The key is knowing when to seek help and what type of professional is right for your situation.

A fee-only financial planner can provide comprehensive retirement planning advice without the potential conflicts of interest that come with commission-based compensation. Look for planners with relevant credentials like CFP (Certified Financial Planner) or ChFC (Chartered Financial Consultant). Many planners offer one-time consultations if you don’t need ongoing management.

Consider working with a tax professional, especially as you approach retirement. Tax planning becomes increasingly important when you’re managing multiple income sources and trying to minimize your lifetime tax burden. A CPA or enrolled agent can help you develop tax-efficient withdrawal strategies and navigate complex rules around required minimum distributions.

Don’t overlook free resources. The Social Security Administration, IRS, and Department of Labor all provide extensive educational materials about retirement planning. Many employers offer retirement planning seminars or access to financial wellness programs. Online calculators and planning tools can help you model different scenarios and understand the impact of various decisions.

Conclusion

Assessing your retirement readiness isn’t a one-and-done exercise – it’s an ongoing process that should be revisited regularly as your circumstances change. Life has a way of throwing curveballs, whether it’s a job loss, health issue, market downturn, or unexpected windfall. The key is to stay flexible and adjust your plan as needed while maintaining focus on your long-term goals.

Remember, the perfect retirement plan doesn’t exist. What matters is having a plan that works for your unique situation and gives you confidence that you can maintain your desired lifestyle throughout your golden years. Start where you are, use what you have, and do what you can. Even small steps taken consistently over time can lead to significant improvements in your retirement readiness.

The most important step is the first one. Whether you’re thrilled with what you discovered during your assessment or concerned about gaps in your preparation, you now have a clearer picture of where you stand. Use this knowledge as motivation to take action, seek professional guidance when needed, and stay committed to your retirement goals. Your future self will thank you for the effort you put in today.