Understanding the Benefits of the 529 College Savings Plan: Your Complete Guide to Smart Education Funding

As college tuition costs continue to soar year after year, parents across the country are scrambling to find effective ways to save for their children’s higher education. If you’ve been losing sleep over how you’ll afford your child’s college expenses, you’re not alone. The good news? There’s a powerful financial tool that can help ease this burden: the 529 college savings plan.

Named after Section 529 of the Internal Revenue Code, these education savings accounts have become increasingly popular among families who want to get ahead of rising education costs. But what exactly makes a 529 plan so special, and how can it benefit your family’s financial future? Let’s dive deep into everything you need to know about this valuable savings vehicle.

What Exactly Is a 529 College Savings Plan?

A 529 plan is a tax-advantaged investment account specifically designed to encourage saving for future education costs. Think of it as a specialized savings account that grows over time, similar to a 401(k) retirement plan, but with education as the primary focus. These plans are sponsored by states, state agencies, or educational institutions and come in two main varieties: education savings plans and prepaid tuition plans.

The beauty of a 529 plan lies in its flexibility and tax benefits. While you contribute after-tax dollars to the account, your money grows tax-free, and withdrawals for qualified education expenses are also tax-free at the federal level. This triple tax advantage makes 529 plans one of the most efficient ways to save for college expenses.

The Compelling Tax Advantages That Make 529 Plans Shine

When it comes to tax benefits, 529 plans are hard to beat. The most significant advantage is the tax-free growth of your investments. Unlike regular savings accounts where you pay taxes on interest earned, or taxable investment accounts where you owe taxes on gains, your 529 plan investments can grow completely tax-free for years or even decades.

Additionally, when you withdraw money to pay for qualified education expenses, those withdrawals are completely tax-free at the federal level. This means that if your account grows from $50,000 to $100,000 over 18 years, you won’t owe a penny in federal taxes on that $50,000 in growth when you use it for education expenses.

Many states sweeten the deal even further by offering state income tax deductions or credits for contributions to their 529 plans. Some states allow you to deduct the full amount of your annual contribution, while others cap the deduction at a certain amount. It’s worth researching your state’s specific benefits, as they can add up to substantial savings over time.

Investment Growth Potential and Compound Interest Magic

One of the most powerful aspects of 529 plans is their potential for long-term investment growth. Most plans offer a variety of investment options, from conservative money market funds to aggressive stock portfolios. Many plans also feature age-based investment tracks that automatically adjust your portfolio to become more conservative as your child approaches college age.

The magic of compound interest really shines in 529 plans. When you start saving early, even small monthly contributions can grow into substantial amounts by the time your child reaches college age. For example, if you contribute $200 per month starting when your child is born and earn an average annual return of 6%, you could have over $80,000 saved by the time they turn 18.

This growth potential is particularly important given the rising cost of higher education. By investing in a diversified portfolio through your 529 plan, you’re giving your savings the best chance to keep pace with or even exceed tuition inflation over the long term.

Flexibility in Usage: More Than Just Tuition

Gone are the days when 529 plans could only be used for traditional four-year college expenses. Recent changes to federal law have significantly expanded what qualifies as an eligible education expense, making these plans more flexible than ever before.

Qualified expenses now include tuition and fees, room and board, books and supplies, computers and related technology, and even internet access. The plans can be used at eligible institutions nationwide, including colleges, universities, vocational schools, and other post-secondary educational institutions.

Perhaps most importantly, you can now use up to $10,000 per year from a 529 plan to pay for K-12 tuition at private, public, or religious schools. This expansion has made 529 plans valuable for families considering private elementary or high school education for their children.

Additionally, recent legislation allows 529 funds to be used for qualified student loan repayments (up to $10,000 lifetime limit per beneficiary) and certain apprenticeship program expenses, further increasing the plan’s versatility.

High Contribution Limits and No Income Restrictions

Unlike many other tax-advantaged accounts, 529 plans don’t have annual contribution limits set by federal law. Instead, each state sets its own maximum account balance, which typically ranges from $300,000 to over $500,000 per beneficiary. This means you can contribute substantial amounts if you have the financial means to do so.

For gift tax purposes, you can contribute up to the annual gift tax exclusion amount (currently $17,000 for 2023) per beneficiary without triggering gift tax consequences. Even better, 529 plans offer a unique “superfunding” option that allows you to contribute up to five years’ worth of annual exclusions at once (currently $85,000) without gift tax implications, provided you don’t make additional gifts to that beneficiary during the five-year period.

Another significant advantage is that 529 plans have no income restrictions. Whether you earn $50,000 or $500,000 per year, you can still take advantage of all the benefits these plans offer. This makes them accessible to families across all income levels.

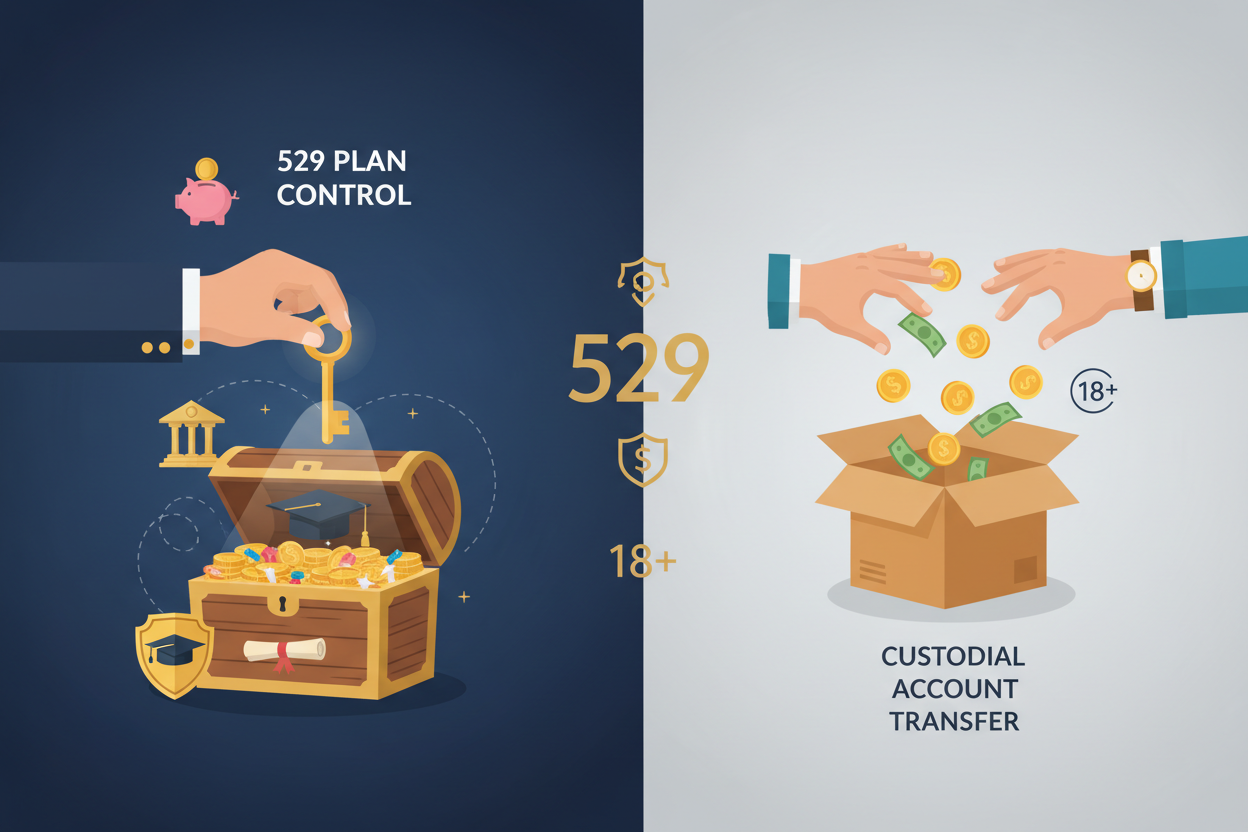

Control and Ownership Benefits

As the account owner of a 529 plan, you maintain complete control over the funds, even after your child reaches adulthood. This is different from custodial accounts, where control transfers to the child at the age of majority. With a 529 plan, you decide when and how the money is distributed, giving you peace of mind that the funds will be used for their intended purpose.

You also have the flexibility to change the beneficiary to another qualifying family member if your original beneficiary doesn’t need the funds for education. This could include siblings, cousins, or even yourself if you decide to go back to school. This flexibility ensures that your education savings don’t go to waste if circumstances change.

The account owner can also change investment options within the plan, typically once per calendar year or when changing beneficiaries. This allows you to adjust your investment strategy as your child grows older or as market conditions change.

Minimal Impact on Financial Aid

When it comes to college financial aid calculations, 529 plans are treated relatively favorably compared to other types of savings. If the account is owned by a parent, it’s considered a parental asset and assessed at a maximum rate of 5.64% in the Expected Family Contribution calculation used for federal financial aid.

This is much more favorable than assets held directly in a student’s name, which are assessed at 20%. Additionally, qualified withdrawals from parent-owned 529 plans are not counted as student income, which could otherwise significantly impact aid eligibility in subsequent years.

For families concerned about financial aid impact, the relatively gentle treatment of 529 plans makes them a smart choice compared to other savings vehicles like custodial accounts or savings bonds held in a child’s name.

Getting Started: Choosing the Right 529 Plan

With so many 529 plans available, choosing the right one can feel overwhelming. You’re not limited to your home state’s plan, so it’s worth comparing options from different states. Key factors to consider include investment options, fees and expenses, performance history, and any state tax benefits available to you.

Many financial experts recommend looking at plans from states like Utah, Nevada, and New York, which are known for their low fees and strong investment options, even if you don’t live in those states. However, if your home state offers significant tax benefits for contributions, it might make sense to stick with your state’s plan despite potentially higher fees.

You can open a 529 plan directly with the plan provider, through a financial advisor, or sometimes through payroll deduction if your employer offers this benefit. Many plans have low minimum initial contributions, making it easy to get started even if you can only save small amounts initially.

Maximizing Your 529 Plan Strategy

To get the most out of your 529 plan, start saving as early as possible, even if you can only contribute small amounts initially. The power of compound growth means that money invested when your child is young has the most time to grow. Consider setting up automatic contributions to make saving effortless and consistent.

Don’t forget to involve family members in your 529 plan strategy. Grandparents, aunts, uncles, and family friends can all contribute to your child’s 529 plan, making it a great alternative to traditional gifts for birthdays and holidays. Many plans offer gifting platforms that make it easy for family members to contribute.

Finally, review and adjust your investment strategy periodically. As your child gets closer to college age, you may want to shift to more conservative investments to protect your accumulated savings from market volatility.

Conclusion: Your Path to Education Funding Success

The 529 college savings plan represents one of the most powerful tools available for education funding. With its combination of tax-free growth, flexible usage options, high contribution limits, and minimal impact on financial aid, it’s no wonder that these plans have become the gold standard for education savings.

While the rising cost of higher education can feel daunting, starting a 529 plan gives you a concrete way to take control of your family’s educational future. Whether you’re able to contribute $25 per month or $500 per month, the key is to start now and let time work in your favor.

Remember, every dollar you save today in a 529 plan is a dollar your child won’t need to borrow tomorrow. In a world where student loan debt has reached crisis levels, giving your child the gift of a debt-free education start is one of the most valuable presents you can provide. Take the first step today by researching 529 plans in your area and opening an account that will serve your family for years to come.