Comparing IRA and Roth IRA: Which Option Fits Your Needs?

Planning for retirement can feel overwhelming, especially when you’re faced with alphabet soup of investment options. Two of the most popular retirement savings vehicles – Traditional IRAs and Roth IRAs – often leave people scratching their heads. While both are Individual Retirement Accounts designed to help you build wealth for your golden years, they work in fundamentally different ways.

The choice between a Traditional IRA and Roth IRA isn’t just about picking one over the other – it’s about understanding how each aligns with your current financial situation, future goals, and tax strategy. Think of it like choosing between paying for a meal now or later, except the “meal” is your tax bill, and the timing could save or cost you thousands of dollars over your lifetime.

In this comprehensive guide, we’ll break down everything you need to know about Traditional and Roth IRAs, helping you make an informed decision that could significantly impact your financial future. Whether you’re just starting your career or approaching retirement, understanding these options is crucial for maximizing your retirement savings.

Understanding Traditional IRAs: The Classic Approach

Traditional IRAs have been around since 1974, making them the original individual retirement account. The concept is straightforward: you contribute money now, get a tax deduction today, and pay taxes when you withdraw the funds in retirement. It’s like getting a discount on your taxes now in exchange for paying full price later.

When you contribute to a Traditional IRA, you’re essentially making a deal with the IRS. You reduce your current taxable income by the amount you contribute (up to annual limits), which can lower your tax bill today. However, every dollar you withdraw in retirement – including both your contributions and any growth – gets taxed as ordinary income.

The appeal of Traditional IRAs becomes clear when you consider that many people find themselves in lower tax brackets during retirement than during their peak earning years. If you’re currently in a high tax bracket and expect to be in a lower one when you retire, the Traditional IRA’s tax-deferred structure could work in your favor.

Roth IRA Basics: Pay Now, Benefit Later

Roth IRAs, introduced in 1997, flip the Traditional IRA concept on its head. Named after Senator William Roth Jr., these accounts require you to pay taxes on your contributions upfront, but offer tax-free withdrawals in retirement. Think of it as paying full price for your meal now so you can eat for free later.

With a Roth IRA, you contribute after-tax dollars, meaning you don’t get an immediate tax deduction. However, once your money is in the account, it grows tax-free, and qualified withdrawals in retirement are completely tax-free. This includes both your original contributions and all the investment growth over the years.

The Roth IRA’s tax-free growth potential becomes particularly powerful over long time horizons. A 25-year-old who contributes to a Roth IRA has potentially 40+ years for their investments to grow without ever owing taxes on that growth again. For younger investors or those who expect to be in higher tax brackets in retirement, this can be incredibly valuable.

Key Differences in Contribution Rules and Limits

While both account types have annual contribution limits, the rules surrounding who can contribute and how much differ significantly. For 2024, both Traditional and Roth IRAs have the same contribution limits: $7,000 for those under 50, and $8,000 for those 50 and older (thanks to the catch-up contribution).

However, eligibility and deductibility rules create important distinctions. Traditional IRA contributions may be tax-deductible depending on your income level and whether you have access to an employer-sponsored retirement plan. If you’re covered by a 401(k) at work, your ability to deduct Traditional IRA contributions phases out at certain income levels.

Roth IRAs have their own income restrictions, but they work differently. High earners may be completely prohibited from contributing directly to a Roth IRA. For 2024, the phase-out begins at $138,000 for single filers and $218,000 for married couples filing jointly. However, there’s a workaround called the “backdoor Roth conversion” that high earners often use, though it requires careful planning and professional guidance.

Tax Implications: When and How You Pay

The tax treatment difference between Traditional and Roth IRAs is perhaps the most critical factor in your decision. With Traditional IRAs, you’re essentially borrowing money from the government in the form of tax deductions, with the understanding that you’ll pay it back (with interest, in the form of taxes on growth) later.

Consider this example: if you’re in the 22% tax bracket and contribute $6,000 to a Traditional IRA, you could save $1,320 in taxes that year. However, if that $6,000 grows to $60,000 over 30 years, you’ll owe taxes on the entire $60,000 when you withdraw it in retirement.

With a Roth IRA, you pay taxes on that same $6,000 contribution upfront, but the entire $60,000 (using the same growth assumption) would be yours tax-free in retirement. The question becomes: would you rather pay taxes on $6,000 today or $60,000 in the future? The answer depends largely on your current versus expected future tax rates.

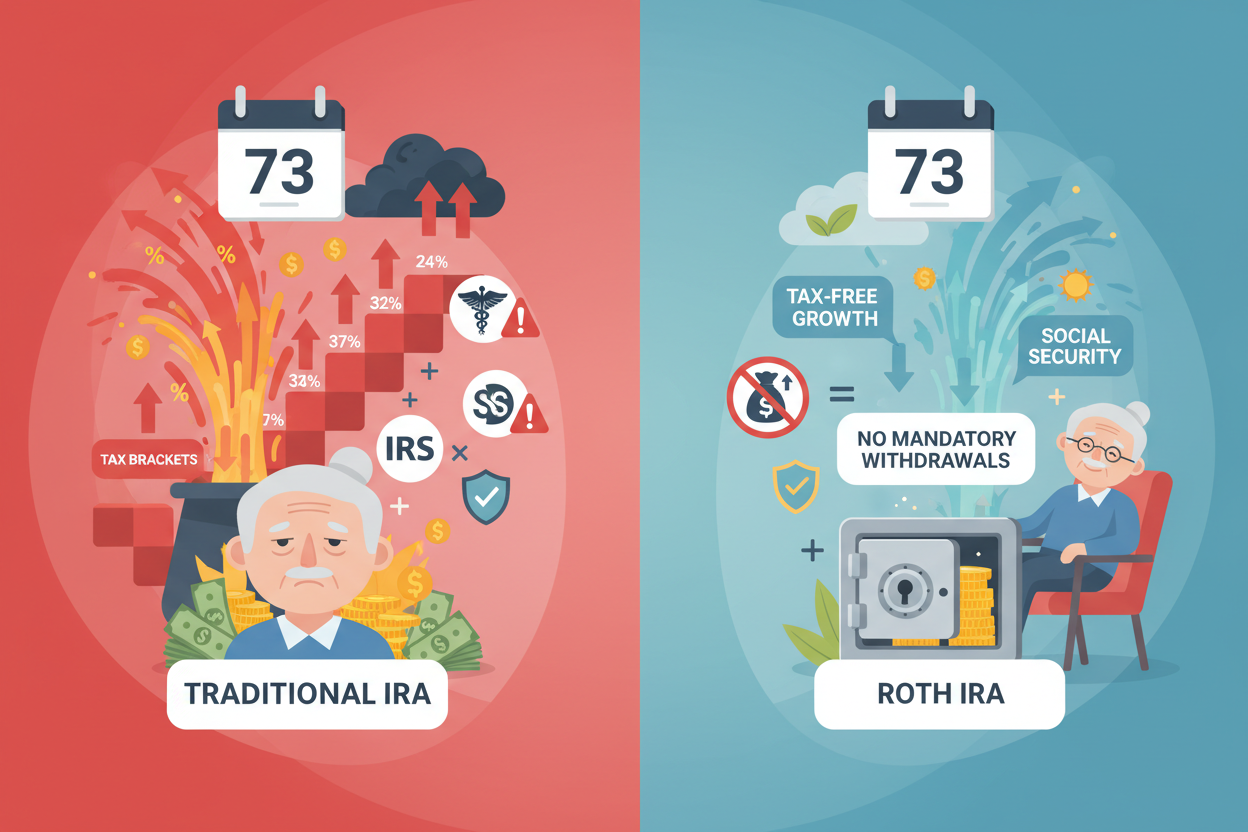

Required Minimum Distributions: A Critical Difference

One of the most significant advantages of Roth IRAs becomes apparent later in life: Required Minimum Distributions, or RMDs. Traditional IRAs require you to start taking withdrawals at age 73, whether you need the money or not. This forced distribution can push you into higher tax brackets and may affect other aspects of your financial life, such as Medicare premiums or Social Security taxation.

Roth IRAs, on the other hand, have no RMDs during the original owner’s lifetime. This means your money can continue growing tax-free for as long as you live, making Roth IRAs excellent tools for wealth transfer to heirs. You can leave your Roth IRA untouched if you don’t need the money, allowing it to serve as a legacy for your beneficiaries.

This difference makes Roth IRAs particularly attractive for individuals who have other sources of retirement income and want to minimize their tax burden in later years. It also provides more flexibility in retirement income planning, as you can choose when and how much to withdraw without government mandates.

Age and Career Stage Considerations

Your age and career stage play crucial roles in determining which IRA type makes more sense. Younger workers, particularly those early in their careers, often benefit more from Roth IRAs. They’re typically in lower tax brackets now than they expect to be in the future, making it advantageous to pay taxes at today’s lower rates.

Additionally, younger investors have the most valuable asset on their side: time. The longer your money has to grow tax-free in a Roth IRA, the more powerful the tax-free compounding becomes. A 25-year-old contributing to a Roth IRA has potentially 40+ years for their investments to grow without ever owing taxes on that growth again.

Mid-career professionals often face a more complex decision. They may be in their peak earning years, making Traditional IRA deductions more valuable, but they also have substantial time for Roth IRA growth. Many financial advisors suggest a diversified approach, contributing to both types of accounts to create tax diversification in retirement.

For those closer to retirement, Traditional IRAs might make more sense if they expect to be in lower tax brackets in retirement. However, if they have adequate other retirement savings and want to minimize RMDs or leave tax-free inheritances, Roth conversions might be worth considering.

Income Level Impact on Your Decision

Your current income level significantly influences which IRA option works best for your situation. High earners in peak tax brackets often benefit from the immediate tax deduction of Traditional IRAs, especially if they expect their retirement income to be lower than their current income.

However, high earners face contribution restrictions for Roth IRAs and may lose the deductibility of Traditional IRA contributions if they have employer-sponsored retirement plans. This is where strategies like the backdoor Roth conversion come into play, though these require careful planning to avoid tax pitfalls.

Lower and moderate-income earners might find Roth IRAs more attractive, particularly if they’re eligible for the Saver’s Credit, which can provide additional tax benefits for retirement contributions. The Saver’s Credit is a tax credit (not just a deduction) that can be worth up to $1,000 for individuals or $2,000 for married couples, making Roth contributions even more valuable.

Flexibility and Accessibility Differences

Roth IRAs offer more flexibility when it comes to accessing your money before retirement. You can withdraw your contributions (but not earnings) at any time without taxes or penalties, since you’ve already paid taxes on that money. This makes Roth IRAs somewhat dual-purpose, serving as both retirement accounts and emergency funds, though using them for emergencies isn’t ideal for long-term wealth building.

Traditional IRAs are less flexible for early access. Withdrawals before age 59½ typically incur a 10% penalty plus income taxes, though there are exceptions for certain circumstances like first-time home purchases, higher education expenses, or medical emergencies.

This flexibility makes Roth IRAs particularly attractive for younger investors who might worry about tying up their money for decades. However, it’s important to resist the temptation to raid your retirement savings for non-retirement purposes, as doing so significantly impacts your long-term wealth accumulation.

Making Your Decision: Factors to Consider

Choosing between a Traditional and Roth IRA isn’t always an either-or decision. Many financial advisors recommend a balanced approach, contributing to both types of accounts to create tax diversification in retirement. This strategy gives you flexibility to manage your tax burden in retirement by choosing which accounts to withdraw from based on your tax situation each year.

Consider your current tax bracket versus your expected retirement tax bracket. If you’re currently in a high tax bracket and expect to be in a lower one in retirement, Traditional IRAs might make more sense. If you’re in a lower bracket now or expect to be in a higher one in retirement, Roth IRAs could be more beneficial.

Think about your retirement timeline and goals. If you’re young with decades until retirement, the tax-free growth potential of Roth IRAs becomes more compelling. If you’re closer to retirement and need the immediate tax deduction, Traditional IRAs might be more appropriate.

Don’t forget to consider your overall financial picture. If you have substantial assets in tax-deferred accounts like 401(k)s, adding Roth IRA contributions can provide valuable tax diversification. Conversely, if most of your retirement savings are in Roth accounts, some Traditional IRA contributions might help balance your tax situation.

Conclusion

The choice between Traditional and Roth IRAs ultimately depends on your unique financial situation, goals, and expectations about future tax rates. Both are powerful tools for building retirement wealth, but they work best for different circumstances and life stages.

Remember that this decision isn’t permanent – you can change your contribution strategy as your circumstances evolve, and you can even convert Traditional IRA funds to Roth IRAs (though this triggers a taxable event). The most important thing is to start saving for retirement as early as possible, regardless of which account type you choose.

Consider consulting with a financial advisor or tax professional who can analyze your specific situation and help you develop a comprehensive retirement savings strategy. They can help you navigate the complexities of contribution limits, income restrictions, and tax implications to ensure you’re making the most of these valuable retirement planning tools.

The key takeaway? Don’t let the complexity of choosing between Traditional and Roth IRAs prevent you from saving for retirement. Both options are significantly better than not saving at all, and starting early – even with the “wrong” choice – is better than waiting for the perfect decision. Your future self will thank you for taking action today, regardless of which path you choose.