The Importance of Financial Wellness Planning for Families: Building a Secure Future Together

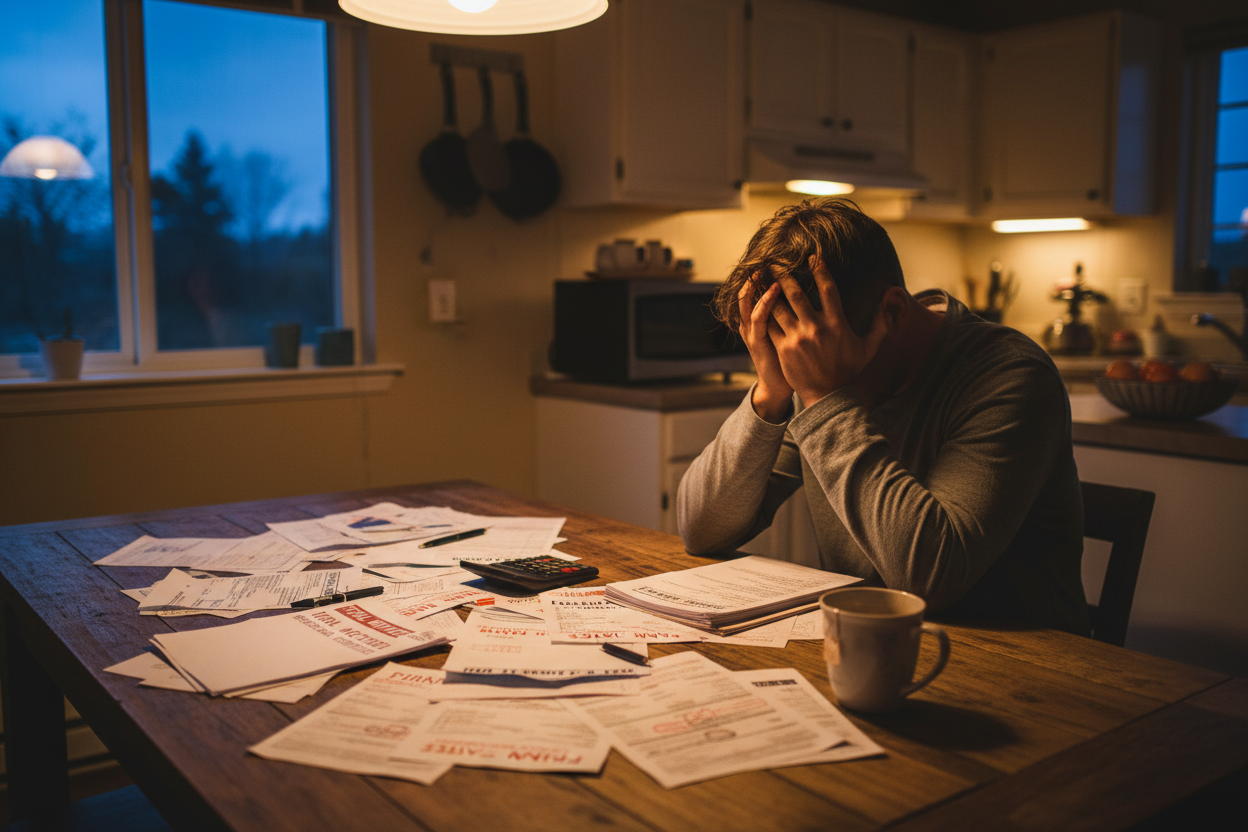

Picture this: It’s Sunday evening, and you’re sitting at the kitchen table surrounded by bills, bank statements, and a growing sense of anxiety about your family’s financial future. Sound familiar? You’re not alone. Millions of families across the country struggle with financial stress, often because they lack a comprehensive financial wellness plan. But here’s the good news – it doesn’t have to be this way.

Financial wellness planning isn’t just about having money in the bank or paying bills on time. It’s about creating a holistic approach to managing your family’s finances that promotes peace of mind, security, and the ability to achieve your dreams together. When families take control of their financial health, they’re not just securing their present – they’re building a foundation for generations to come.

What Is Financial Wellness Planning and Why Does It Matter?

Financial wellness planning goes beyond traditional budgeting or saving money. It’s a comprehensive approach that encompasses your family’s entire financial ecosystem – from daily spending habits to long-term investment strategies. Think of it as a roadmap that guides your family through various life stages, unexpected challenges, and exciting opportunities.

The beauty of financial wellness planning lies in its personalized nature. What works for your neighbor’s family might not work for yours, and that’s perfectly okay. Your plan should reflect your family’s unique values, goals, and circumstances. Maybe your priority is saving for your children’s education, or perhaps you’re focused on paying off debt while building an emergency fund. Whatever your situation, a well-crafted financial wellness plan serves as your North Star.

Research consistently shows that families with solid financial plans experience less stress, better relationships, and improved overall well-being. When money isn’t a constant source of worry, families can focus on what truly matters – spending quality time together, pursuing passions, and creating lasting memories.

The Foundation: Emergency Funds and Debt Management

Before you can build a castle, you need solid ground to stand on. In financial wellness planning, that foundation consists of two critical elements: emergency funds and debt management. These aren’t the most exciting aspects of financial planning, but they’re absolutely essential for your family’s long-term success.

An emergency fund acts as your family’s financial safety net. Life has a way of throwing curveballs – unexpected medical bills, car repairs, or job loss can derail even the best-laid plans. Financial experts typically recommend saving three to six months’ worth of living expenses, but don’t let this number intimidate you. Start small, perhaps with a goal of $1,000, and gradually build from there.

Debt management is equally crucial. High-interest debt, particularly credit card debt, can quickly spiral out of control and sabotage your family’s financial goals. Consider strategies like the debt snowball method, where you pay off smallest debts first to build momentum, or the debt avalanche approach, which targets high-interest debt first to minimize total interest paid.

Remember, building your foundation takes time, and that’s completely normal. Celebrate small victories along the way – every dollar saved and every debt payment made is a step toward greater financial wellness for your family.

Setting Family Financial Goals That Actually Work

Goal setting in family financial planning is where dreams meet reality. It’s one thing to say you want to “save more money” and entirely another to establish specific, measurable objectives that your entire family can rally around. The most effective family financial goals are those that resonate with everyone and reflect your shared values.

Start by having honest conversations with your family members about what matters most to each person. Your teenager might prioritize saving for a car, while you and your spouse focus on retirement planning. The key is finding ways to balance individual desires with collective family needs.

Short-term goals might include building that emergency fund, paying off a credit card, or saving for a family vacation. Medium-term goals could involve saving for a down payment on a house or funding your children’s college education. Long-term goals typically center around retirement planning and legacy building.

Make your goals specific and time-bound. Instead of “save for vacation,” try “save $3,000 for our Disney World trip by next December.” This specificity makes the goal feel more achievable and provides clear benchmarks for measuring progress. Consider creating a visual representation of your goals – a chart on the refrigerator or a family vision board can serve as daily motivation.

Teaching Financial Literacy to Children

One of the greatest gifts you can give your children is financial literacy. In our increasingly complex financial world, children who understand money management principles have a significant advantage as they navigate adulthood. The earlier you start these conversations, the more natural financial responsibility becomes for your kids.

Age-appropriate financial education looks different at every stage. Young children can learn basic concepts through allowances and saving for small purchases. As they grow, introduce concepts like budgeting, comparison shopping, and the difference between needs and wants. Teenagers can benefit from learning about credit, student loans, and even basic investing principles.

Make financial education practical and engaging. Take children grocery shopping and explain how you make purchasing decisions. Let them help plan a family budget or save for a shared goal. When they receive money as gifts, encourage them to divide it into categories: spending, saving, and giving. These hands-on experiences create lasting impressions that textbook learning simply can’t match.

Consider opening savings accounts for your children and teaching them about interest and compound growth. Many banks offer special youth accounts with educational resources and tools designed specifically for young savers. Watching their money grow, even by small amounts, helps children understand the power of saving and patience.

Investment Strategies for Long-Term Family Security

Once your family has established a solid foundation with emergency savings and manageable debt, it’s time to think about growing your wealth through strategic investing. Investment planning for families requires balancing growth potential with risk management, always keeping your family’s timeline and risk tolerance in mind.

Diversification remains one of the most important principles in family investment planning. Rather than putting all your eggs in one basket, spread investments across different asset classes, industries, and geographical regions. This approach helps protect your family’s wealth during market volatility while still allowing for long-term growth.

Consider tax-advantaged accounts like 401(k)s, IRAs, and 529 education savings plans. These vehicles offer significant benefits for families planning for retirement and education expenses. Many employers offer matching contributions to retirement plans – this is essentially free money that can dramatically accelerate your family’s wealth building.

Don’t overlook the power of dollar-cost averaging, especially when investing for long-term goals. By investing a fixed amount regularly, regardless of market conditions, families can reduce the impact of market volatility and build wealth steadily over time. This strategy works particularly well for busy families who want to automate their investing without constantly monitoring market movements.

Insurance and Protection Planning

While nobody likes to think about worst-case scenarios, protecting your family against potential financial disasters is a cornerstone of comprehensive financial wellness planning. Insurance serves as a crucial safety net that can prevent unexpected events from derailing your family’s financial progress.

Life insurance becomes particularly important when you have dependents counting on your income. Term life insurance often provides the most cost-effective coverage for young families, offering substantial protection during the years when financial obligations are highest. As your children become financially independent and your assets grow, your insurance needs may change accordingly.

Disability insurance protects your family’s most valuable asset – your ability to earn income. Statistics show that workers are more likely to become disabled than to die during their working years, yet many families overlook this critical protection. Both short-term and long-term disability coverage can provide essential income replacement if illness or injury prevents you from working.

Health insurance, property insurance, and umbrella liability coverage round out a comprehensive protection strategy. While insurance premiums represent ongoing expenses, the financial devastation that can result from being underinsured far outweighs these costs. Review your coverage annually to ensure it still meets your family’s evolving needs.

Estate Planning: Securing Your Family’s Future

Estate planning might seem like something only wealthy families need to worry about, but every family with assets or dependents should have basic estate planning documents in place. These legal instruments ensure that your wishes are carried out and your family is protected if something happens to you.

At minimum, every adult should have a will that specifies how assets should be distributed and who should care for minor children. Without a will, state laws determine these crucial decisions, which may not align with your family’s best interests. Powers of attorney for financial and healthcare decisions are equally important, allowing trusted individuals to act on your behalf if you become incapacitated.

For families with more substantial assets, trusts can provide additional benefits including tax advantages, asset protection, and more precise control over how and when beneficiaries receive inheritances. Consider consulting with an estate planning attorney to understand which strategies make sense for your family’s situation.

Don’t forget to regularly update beneficiary designations on retirement accounts, life insurance policies, and other financial accounts. These designations typically supersede instructions in your will, so keeping them current is essential for ensuring your assets go where you intend.

Creating Your Family’s Financial Wellness Action Plan

Now that you understand the key components of financial wellness planning, it’s time to create your family’s personalized action plan. Start by conducting a thorough assessment of your current financial situation. Gather information about all assets, debts, income sources, and expenses. This financial snapshot serves as your starting point.

Next, prioritize your goals based on urgency and importance. While you might want to tackle everything at once, focusing on one or two primary objectives initially will yield better results than spreading your efforts too thin. Perhaps you’ll start with building that emergency fund while simultaneously paying down high-interest debt.

Establish regular family financial meetings to review progress, adjust goals, and address any challenges that arise. These don’t need to be lengthy or formal – even a monthly 30-minute check-in can keep your family on track and ensure everyone remains engaged in the process.

Consider working with financial professionals when appropriate. While many aspects of financial wellness planning can be handled independently, complex situations may benefit from expert guidance. Fee-only financial planners, tax professionals, and estate planning attorneys can provide valuable expertise and objective perspectives.

Financial wellness planning for families isn’t a destination – it’s an ongoing journey that evolves with your family’s changing needs and circumstances. What matters most is taking that first step and committing to the process. Your family’s financial future depends on the decisions you make today, and every small action contributes to building the secure, prosperous future your family deserves.

Remember, perfect is the enemy of good when it comes to financial planning. You don’t need to have everything figured out before you begin. Start where you are, use what you have, and do what you can. Your future self – and your family – will thank you for taking action today.