Financial Help After Divorce: Creating a New Path

Divorce marks the end of one chapter and the beginning of another. While the emotional journey gets plenty of attention, the financial reality often hits harder than expected. Suddenly, you’re managing expenses that were once shared, rebuilding credit that may have been damaged, and planning for a future you never quite envisioned.

The good news? You’re not alone in this journey, and there are concrete steps you can take to regain financial stability. Whether you’re dealing with reduced income, unexpected legal fees, or the challenge of establishing independent credit, creating a solid financial foundation after divorce is entirely possible with the right approach and resources.

Understanding Your New Financial Reality

The first step toward financial recovery involves taking an honest look at where you stand today. This isn’t about dwelling on what was lost, but rather understanding what you’re working with moving forward.

Start by gathering all your financial documents. This includes bank statements, credit reports, investment accounts, and any debt obligations. Many people discover they don’t have a complete picture of their finances during marriage, so this exercise often reveals surprises – both positive and challenging.

Your income has likely changed, and your expenses definitely have. What once felt manageable with two incomes might now seem overwhelming. That’s completely normal. The key is creating a realistic budget that reflects your current situation, not your past lifestyle.

Don’t forget to factor in divorce-related expenses that might continue for months. Legal fees, therapy costs, and the expense of establishing a new household all impact your immediate financial picture. Understanding these costs upfront helps prevent financial surprises down the road.

Government Assistance Programs for Divorced Individuals

Many people feel hesitant about exploring government assistance, but these programs exist precisely for situations like yours. Divorce often creates temporary financial hardship, and utilizing available resources can provide the breathing room needed to rebuild.

The Supplemental Nutrition Assistance Program (SNAP) helps with food costs, which can free up money for other essential expenses. Eligibility is based on your current household size and income, not your previous married status. The application process has become more streamlined, with many states offering online applications.

Housing assistance programs, including Section 8 vouchers and public housing, can significantly reduce your largest monthly expense. While waiting lists exist in many areas, getting your name on the list early is crucial. Some programs specifically prioritize single parents or individuals experiencing housing instability due to domestic situations.

Healthcare coverage through Medicaid or marketplace subsidies becomes especially important if you previously relied on your spouse’s insurance. The loss of coverage qualifies as a special enrollment period, allowing you to secure new coverage outside the typical enrollment window.

Temporary Assistance for Needy Families (TANF) provides cash assistance and job training programs. Each state administers this program differently, but most include provisions for education and skill development that can boost your long-term earning potential.

Building Emergency Funds and Managing Immediate Expenses

Financial experts typically recommend three to six months of expenses in an emergency fund, but after divorce, even a small emergency buffer makes a tremendous difference. Start with a goal of $500 to $1,000 – enough to handle a car repair or medical bill without derailing your entire budget.

Consider opening a separate savings account specifically for emergencies. Many banks offer accounts with no minimum balance requirements, and some even provide small bonuses for setting up automatic transfers. Even saving $25 per week adds up to over $1,300 in a year.

Managing immediate expenses often requires creative solutions. Look for community resources like food banks, clothing closets, and utility assistance programs. These aren’t permanent solutions, but they can provide crucial support during the transition period.

Negotiate with creditors if you’re struggling with existing debt payments. Many companies offer hardship programs that can temporarily reduce payments or interest rates. The key is communicating proactively rather than waiting until you’re behind on payments.

Rebuilding Credit and Managing Debt Post-Divorce

Divorce can wreak havoc on credit scores, especially if joint accounts become delinquent or if you’re suddenly responsible for debts you didn’t fully understand. The first step is obtaining copies of your credit reports from all three major bureaus – you’re entitled to free annual reports from each.

Review every account carefully. Joint accounts that remain open can continue to affect your credit, even if your divorce decree assigns responsibility to your ex-spouse. Consider closing joint accounts or converting them to individual accounts when possible.

If you don’t have credit in your own name, start building it strategically. A secured credit card requires a deposit but functions like a regular credit card for credit-building purposes. Use it for small, regular purchases and pay the balance in full each month.

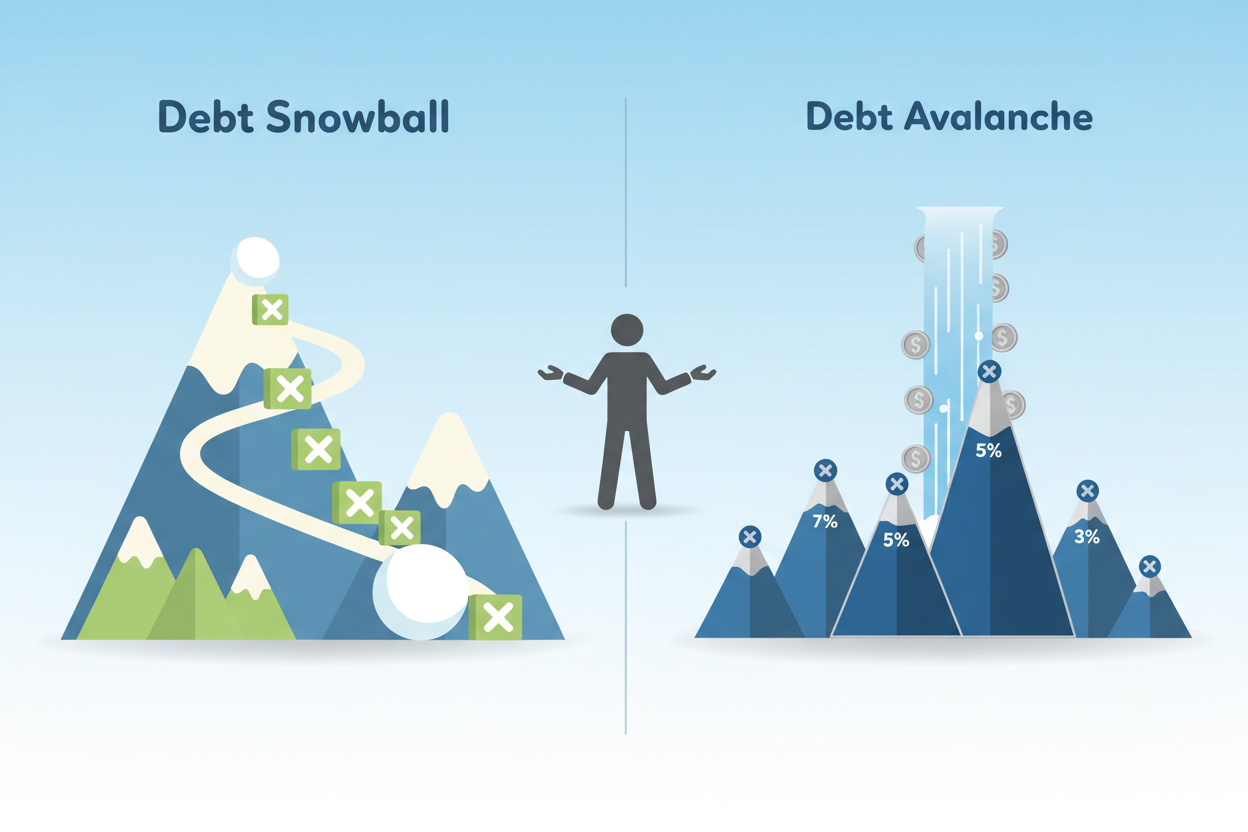

Debt management becomes more challenging on a single income, but several strategies can help. The debt snowball method – paying minimums on all debts while focusing extra payments on the smallest balance – provides psychological wins that maintain motivation. Alternatively, the debt avalanche method targets the highest interest rate debt first, saving money over time.

Consider credit counseling through a nonprofit agency if debt feels overwhelming. These services can help negotiate payment plans and provide education on money management. Avoid for-profit debt settlement companies that often make situations worse.

Exploring Income Opportunities and Career Development

Increasing income often provides the fastest path to financial stability after divorce. This might mean returning to work after time away, changing careers, or developing new skills that command higher wages.

If you’ve been out of the workforce, don’t underestimate the value of your experience. Volunteer work, managing a household, and supporting a spouse’s career all develop transferable skills that employers value. Focus on highlighting these abilities rather than apologizing for employment gaps.

Community colleges and workforce development programs often offer training in high-demand fields. Many programs are designed for working adults and offer evening or weekend classes. Some even provide childcare assistance or transportation vouchers.

The gig economy offers flexible income opportunities that can supplement traditional employment. Driving for rideshare companies, freelance writing, virtual assistance, or selling handmade items online all provide ways to earn money on your schedule.

Don’t overlook remote work opportunities, which have expanded significantly in recent years. Many companies now hire remote customer service representatives, data entry clerks, and administrative assistants. These positions often offer more flexibility for single parents or those managing other responsibilities.

Long-Term Financial Planning and Wealth Building

While immediate financial stability takes priority, thinking about long-term wealth building ensures you’re not just surviving but thriving in your new life. This doesn’t require large amounts of money – even small, consistent efforts compound over time.

Retirement planning becomes more crucial when you can no longer rely on a spouse’s benefits. If your employer offers a 401(k) with matching contributions, prioritize contributing enough to receive the full match – it’s essentially free money. If employer benefits aren’t available, consider opening an IRA with automatic monthly contributions.

Life insurance needs often change after divorce. You might need coverage to protect children or ensure alimony payments continue, or you might be able to reduce coverage and save money. Review beneficiaries on all accounts to reflect your new circumstances.

Estate planning documents require updates after divorce. Wills, power of attorney documents, and healthcare directives should reflect your current wishes. Many states have low-cost legal clinics that can help with basic estate planning needs.

Consider working with a fee-only financial advisor if your situation is complex. These professionals charge for their time rather than earning commissions on products they sell, ensuring their advice serves your best interests.

Finding Community Support and Professional Resources

Financial recovery after divorce doesn’t happen in isolation. Building a support network of professionals and peers can provide both practical assistance and emotional encouragement during challenging times.

Many communities offer divorce support groups that address both emotional and practical concerns. These groups often share resources like recommendations for affordable attorneys, accountants, or financial advisors who understand divorce-related financial challenges.

Local libraries frequently host financial literacy workshops and provide free access to financial planning software and resources. Librarians can help locate government assistance programs and community resources you might not know exist.

Women’s resource centers, even if you’re not a woman, often have information about financial assistance programs and job training opportunities. Many also offer childcare during workshops or meetings, removing a common barrier to accessing help.

Professional organizations in your field might offer networking opportunities or job placement assistance. Many have reduced membership fees for people experiencing financial hardship.

Conclusion

Creating financial stability after divorce requires patience, planning, and often a willingness to ask for help. The path forward might look different from what you originally envisioned, but it can lead to a more secure and independent future.

Remember that financial recovery is rarely linear. There will be setbacks and unexpected expenses, but each step you take toward stability builds momentum for the next. Whether you’re accessing government assistance, building emergency savings, or developing new income streams, you’re actively creating the foundation for your new life.

The skills you develop managing finances independently – budgeting, negotiating, planning, and problem-solving – serve you far beyond the immediate post-divorce period. Many people discover they’re more financially capable than they ever imagined, finding strength and confidence they didn’t know they possessed.

Your financial journey after divorce is uniquely yours, but you don’t have to navigate it alone. Resources exist to help, communities are ready to support you, and with time and effort, you can build the financial security that supports the life you want to create.