Understanding IRA vs. Roth IRA: Tax Implications Explained

When it comes to retirement planning, few decisions are as crucial as choosing between a traditional IRA and a Roth IRA. I’ve seen countless individuals struggle with this choice, and honestly, it’s no wonder why. The tax implications alone can make your head spin, but understanding these differences could save you thousands of dollars in retirement.

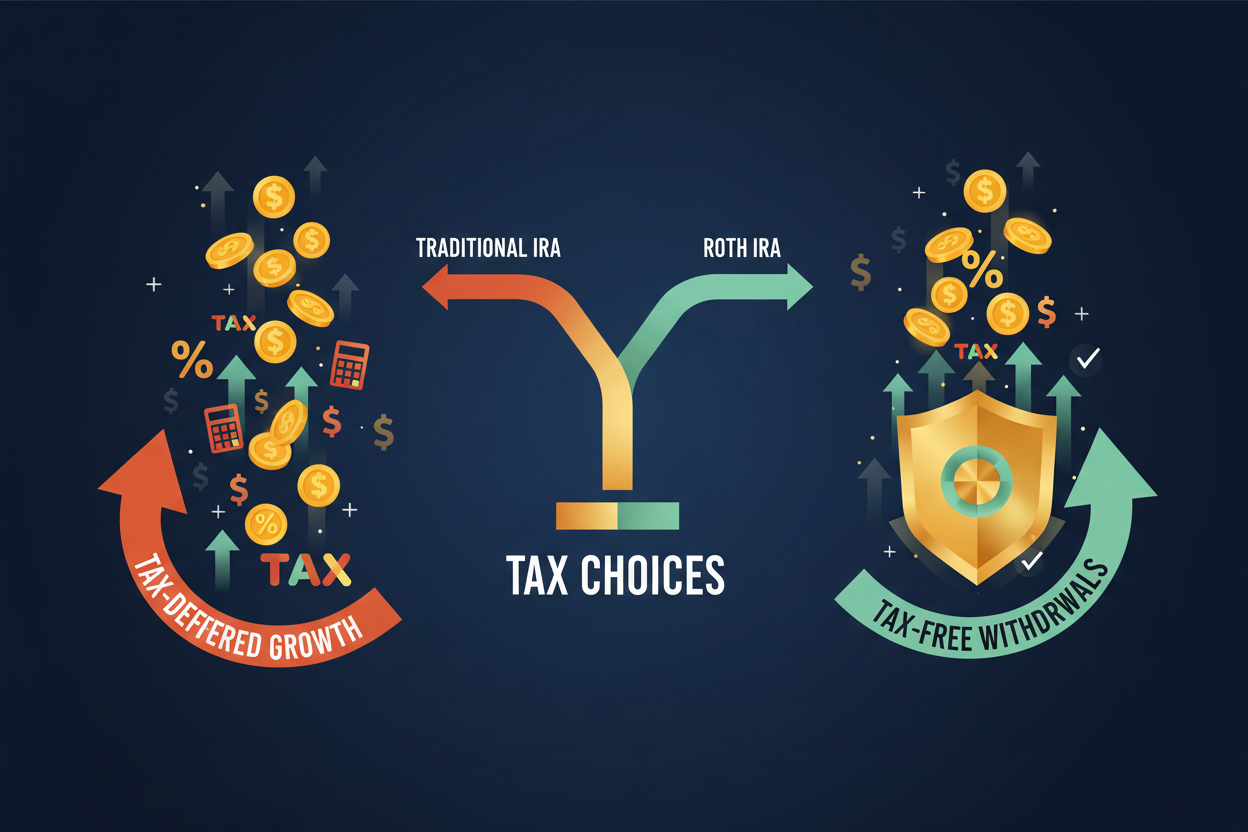

Both IRAs offer powerful tax advantages, but they work in completely opposite ways. Think of it like this: with a traditional IRA, you get your tax break upfront, while with a Roth IRA, you pay taxes now but enjoy tax-free withdrawals later. The question is, which approach makes more sense for your unique financial situation?

Let’s dive deep into the world of IRAs and unpack the tax implications that could significantly impact your retirement nest egg.

What Is a Traditional IRA and How Does It Work?

A traditional Individual Retirement Account (IRA) is like a tax-deferred savings account specifically designed for retirement. When you contribute to a traditional IRA, you’re essentially making a deal with the IRS: you’ll get a tax deduction today, but you’ll pay taxes on both your contributions and earnings when you withdraw the money in retirement.

Here’s how the mechanics work: let’s say you’re in the 22% tax bracket and contribute $6,000 to a traditional IRA. That contribution could reduce your taxable income by $6,000, potentially saving you $1,320 in taxes for that year. Your money then grows tax-deferred until you start taking distributions, typically after age 59½.

The catch? Every penny you withdraw in retirement will be taxed as ordinary income at whatever tax rate you’re facing then. This includes both your original contributions and any investment gains you’ve accumulated over the years.

Roth IRA Fundamentals: The Tax-Free Growth Strategy

A Roth IRA flips the traditional IRA concept on its head. Instead of getting a tax break when you contribute, you pay taxes on your income first, then contribute the after-tax dollars to your Roth IRA. The magic happens during retirement when you can withdraw both your contributions and earnings completely tax-free.

Using the same example as before, if you’re in the 22% tax bracket and want to contribute $6,000 to a Roth IRA, you’ll need to earn about $7,692 in gross income to have $6,000 left after taxes. You won’t get any immediate tax deduction, but that $6,000 can grow for decades without Uncle Sam taking another bite.

The beauty of a Roth IRA becomes apparent in retirement. Whether your account has grown to $50,000 or $500,000, every withdrawal is yours to keep, assuming you follow the rules.

Key Tax Differences Between Traditional and Roth IRAs

The fundamental tax difference between these two retirement accounts comes down to timing. Traditional IRAs offer “tax-deferred” growth, while Roth IRAs provide “tax-free” growth. But the implications run much deeper than this simple distinction.

With traditional IRAs, you’re betting that you’ll be in a lower tax bracket in retirement than you are today. This makes sense for many people, especially high earners who expect their income to drop significantly when they stop working. The immediate tax deduction also provides more money to invest upfront, which can compound over time.

Roth IRAs, on the other hand, work best when you expect to be in the same or higher tax bracket in retirement. This scenario is increasingly common as people live longer, maintain part-time work in retirement, or simply accumulate substantial wealth that generates significant taxable income.

Another crucial difference involves required minimum distributions (RMDs). Traditional IRA owners must start taking distributions at age 73, whether they need the money or not. These forced withdrawals can push retirees into higher tax brackets and trigger additional taxes on Social Security benefits. Roth IRAs have no RMDs during the owner’s lifetime, providing much more flexibility in retirement income planning.

Income Limits and Contribution Restrictions

Not everyone can contribute to both types of IRAs, and understanding these limitations is crucial for tax planning. Traditional IRA contributions are generally available to anyone with earned income, but the tax deductibility phases out at higher income levels if you or your spouse have access to an employer retirement plan.

For 2024, if you’re single and covered by a workplace retirement plan, the traditional IRA deduction begins phasing out at $77,000 in modified adjusted gross income and disappears completely at $87,000. For married couples filing jointly, the phase-out range is $123,000 to $143,000.

Roth IRA eligibility is based purely on income, regardless of workplace plan participation. Single filers can contribute the full amount with incomes up to $138,000, with contributions phasing out between $138,000 and $153,000. For married couples filing jointly, the phase-out range is $218,000 to $228,000.

These income limits create interesting planning opportunities. High earners who can’t contribute directly to a Roth IRA might consider the “backdoor Roth” strategy, where they contribute to a non-deductible traditional IRA and then convert it to a Roth IRA.

When Traditional IRAs Make More Tax Sense

Traditional IRAs shine brightest when you’re currently in a high tax bracket but expect to be in a lower bracket during retirement. This situation is common among peak-earning professionals in their 40s and 50s who plan to have significantly reduced income in retirement.

Consider Sarah, a 45-year-old surgeon earning $400,000 annually. She’s in the 35% tax bracket now, but expects her retirement income to place her in the 22% bracket. Every dollar she contributes to a traditional IRA saves her 35 cents in current taxes, while she’ll only pay 22 cents per dollar in retirement taxes. That’s a 13 percentage point arbitrage opportunity.

Traditional IRAs also make sense when you need the immediate tax deduction to free up cash flow for other financial goals. The upfront tax savings can be redirected toward paying off high-interest debt, building an emergency fund, or investing in taxable accounts.

Additionally, if you’re close to retirement and don’t have decades for tax-free growth to compound, the immediate tax benefit of a traditional IRA might outweigh the long-term advantages of a Roth IRA.

When Roth IRAs Offer Superior Tax Benefits

Roth IRAs typically work best for younger investors and those who expect to be in higher tax brackets in retirement. If you’re in your 20s or 30s and currently in a lower tax bracket, paying taxes now at a relatively low rate can be incredibly advantageous.

Take Mike, a 28-year-old teacher earning $45,000 annually. He’s in the 12% tax bracket now but expects his income to grow significantly over his career. By contributing to a Roth IRA, he locks in today’s low tax rate and ensures that decades of compound growth will never be taxed again.

Roth IRAs also provide unmatched flexibility. Since you’ve already paid taxes on your contributions, you can withdraw them penalty-free at any time for any reason. This makes Roth IRAs excellent emergency funds for young people who might need access to their money before retirement.

For estate planning purposes, Roth IRAs are superior because they don’t require RMDs and pass to heirs tax-free. This makes them powerful wealth transfer vehicles for those who don’t need their retirement savings to fund their own retirement.

Advanced Tax Strategies: Roth Conversions and Tax Diversification

Sophisticated investors often use Roth conversions to optimize their long-term tax situation. This strategy involves moving money from a traditional IRA to a Roth IRA, paying taxes on the converted amount in the year of conversion.

Roth conversions work particularly well during years when your income is temporarily lower, such as early retirement, job transitions, or economic downturns when your traditional IRA balance might be depressed. By converting during these periods, you can fill up lower tax brackets and potentially pay less in total taxes over your lifetime.

Tax diversification is another advanced strategy that involves maintaining both traditional and Roth retirement accounts. This approach provides flexibility in retirement to manage your tax bracket by choosing which accounts to withdraw from based on your annual income needs and tax situation.

For example, you might withdraw from traditional accounts in years when you’re in lower tax brackets and tap Roth accounts when additional income would push you into higher brackets or trigger taxes on Social Security benefits.

Making the Right Choice for Your Financial Future

Choosing between a traditional and Roth IRA isn’t just about current versus future tax rates. Your decision should consider your entire financial picture, including your current income, expected retirement lifestyle, other retirement savings, estate planning goals, and risk tolerance.

If you’re unsure about your future tax bracket, remember that tax diversification can be your friend. Many financial advisors recommend contributing to both types of accounts over your career, especially if your income fluctuates or you expect significant life changes.

The most important thing is to start contributing to some type of retirement account as early as possible. The power of compound growth over decades will likely dwarf the tax differences between these account types. Whether you choose traditional, Roth, or a combination of both, you’ll be far ahead of those who delay saving for retirement.

Remember, these rules and strategies can be complex, and everyone’s situation is unique. Consider consulting with a qualified financial advisor or tax professional who can analyze your specific circumstances and help you develop a personalized retirement savings strategy that maximizes your after-tax wealth in retirement.