Rebuilding Financial Stability After Divorce: A Guide to Your Fresh Start

Divorce isn’t just an emotional upheaval—it’s a complete financial reset that can leave you feeling overwhelmed and uncertain about your future. Whether you initiated the divorce or found yourself on the receiving end, the reality remains the same: your financial landscape has fundamentally changed, and it’s time to rebuild from the ground up.

The good news? While this journey might feel daunting, thousands of people successfully reconstruct their financial lives after divorce every year. With the right strategies, mindset, and patience, you can emerge from this transition stronger and more financially secure than before. This comprehensive guide will walk you through every crucial step of rebuilding your financial stability, from taking stock of your current situation to planning for long-term prosperity.

Taking Stock: Assessing Your Post-Divorce Financial Reality

Before you can chart a course forward, you need to understand exactly where you stand financially. This assessment phase is crucial, even though it might feel uncomfortable to confront the numbers head-on.

Start by gathering all your financial documents—bank statements, investment accounts, retirement funds, insurance policies, and any debt statements. Create a comprehensive list of your assets and liabilities. Remember, this isn’t about dwelling on what you’ve lost; it’s about understanding your new starting point.

Calculate your net worth by subtracting your total debts from your total assets. Don’t panic if the number isn’t what you hoped for—this is simply your baseline. Many people discover that their financial picture, while different, isn’t as dire as they initially feared.

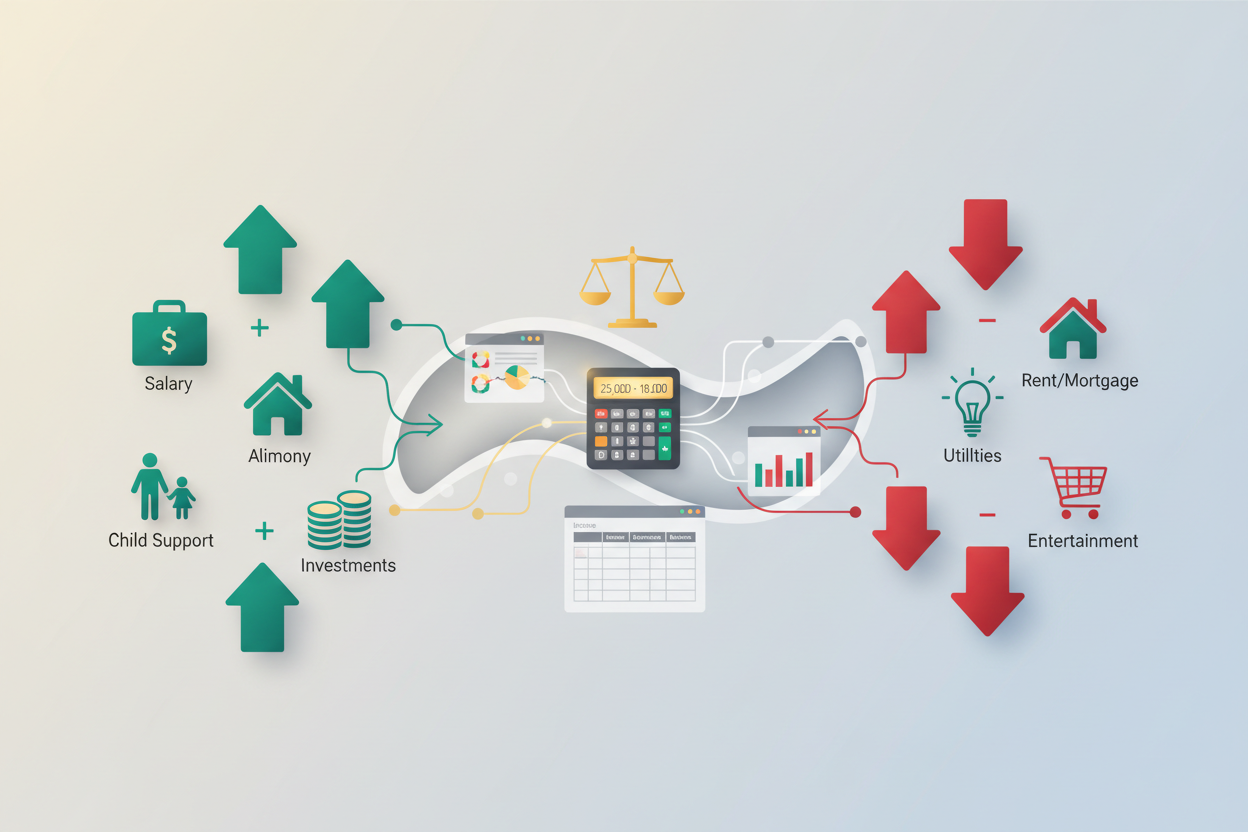

Next, examine your monthly cash flow. List all sources of income, including your salary, alimony, child support, or any other regular payments. Then document your monthly expenses, from housing and utilities to groceries and entertainment. This exercise will reveal whether you’re operating at a surplus or deficit and help identify areas where adjustments might be necessary.

Creating Your New Budget: The Foundation of Financial Recovery

Your pre-divorce budget is now obsolete. Creating a new budget tailored to your current circumstances is perhaps the most important step in rebuilding financial stability. This isn’t about restricting yourself—it’s about taking control and making intentional decisions about your money.

Start with the 50/30/20 rule as a framework, but adjust it to fit your situation. Allocate 50% of your after-tax income to needs (housing, utilities, groceries, minimum debt payments), 30% to wants (dining out, hobbies, entertainment), and 20% to savings and debt repayment beyond minimums.

However, your percentages might look different initially. If you’re dealing with significant debt from the divorce or need to rebuild your emergency fund, you might temporarily allocate more toward debt repayment and savings while reducing discretionary spending.

Be realistic about your expenses, but also be honest about areas where you can cut back. Maybe you don’t need that premium cable package anymore, or perhaps you can find a more affordable gym membership. Small changes can add up to significant savings over time.

Consider using budgeting apps or spreadsheets to track your spending. Many people find that simply monitoring where their money goes each month helps them make better financial decisions automatically.

Rebuilding Your Emergency Fund: Your Financial Safety Net

If divorce depleted your emergency savings, rebuilding this fund should be a top priority. Financial experts typically recommend having three to six months of living expenses saved, but after a divorce, even $1,000 can provide crucial peace of mind while you work toward that larger goal.

Start small and be consistent. Even setting aside $25 or $50 per week can build momentum. Consider opening a separate high-yield savings account specifically for your emergency fund—this keeps the money accessible but separate from your everyday spending account.

Look for opportunities to accelerate your emergency fund growth. Tax refunds, bonuses, or unexpected windfalls should go directly into this account until you reach your target amount. You might also consider temporarily taking on a side hustle or selling items you no longer need to boost your savings rate.

Remember, this fund is truly for emergencies—job loss, medical expenses, or major home repairs. Having this buffer will prevent you from relying on credit cards or loans when unexpected expenses arise, protecting the financial progress you’re working so hard to achieve.

Managing and Eliminating Debt Strategically

Divorce often leaves people with more debt than they had as a married couple, whether from legal fees, the division of marital debt, or the costs of establishing a new household. Developing a strategic approach to debt elimination is crucial for long-term financial health.

First, list all your debts, including the balance, minimum payment, and interest rate for each. This gives you a clear picture of what you’re dealing with and helps you prioritize your repayment strategy.

Consider using either the debt snowball or debt avalanche method. The snowball method involves paying minimums on all debts while putting extra money toward the smallest balance first. This approach provides psychological wins that can keep you motivated. The avalanche method focuses on paying off the highest interest rate debt first, which saves money over time.

If you have high-interest credit card debt, explore options like balance transfers to lower-interest cards or personal loans with better terms. However, be cautious about taking on new credit products unless you’re confident in your ability to manage them responsibly.

Don’t ignore the possibility of negotiating with creditors, especially if you’re struggling to make payments. Many companies would rather work out a payment plan than deal with a default, and they might be willing to reduce interest rates or settle for less than the full amount owed.

Reestablishing Your Credit Profile

Your credit score might have taken a hit during the divorce process, especially if joint accounts were closed or if there were missed payments during the transition. Rebuilding your credit is essential for future financial opportunities like buying a home, getting favorable loan terms, or even securing certain jobs.

Start by obtaining free copies of your credit reports from all three major credit bureaus. Review them carefully for any errors or accounts that should have been removed as part of your divorce settlement. Dispute any inaccuracies immediately, as these can significantly impact your score.

If you don’t have credit cards in your name only, consider applying for one or two. If your credit is damaged, you might need to start with a secured credit card, which requires a deposit but functions like a regular credit card. Use these cards sparingly and pay the full balance each month to demonstrate responsible credit usage.

Keep your credit utilization low—ideally under 30% of your available credit limits, but under 10% is even better. This means if you have a $1,000 credit limit, try to keep your balance below $100.

Be patient with credit rebuilding. It takes time to see significant improvements, but consistent, responsible behavior will gradually raise your score. Avoid the temptation to apply for multiple credit accounts quickly, as this can actually hurt your score in the short term.

Planning for Retirement: It’s Never Too Late to Start Over

Divorce often disrupts retirement planning, whether through the division of retirement assets or simply the need to redirect funds toward immediate expenses. However, it’s crucial not to let retirement planning fall by the wayside, even if you feel like you’re starting from scratch.

If you received retirement assets as part of your divorce settlement, resist the urge to cash them out for immediate needs unless absolutely necessary. The tax penalties and lost compound growth can significantly impact your long-term financial security.

Take advantage of any employer-sponsored retirement plans, especially if there’s a company match—this is essentially free money. If you can’t afford to contribute much initially, start with whatever amount gets you the full company match, then gradually increase your contributions as your financial situation improves.

Consider opening an IRA if you don’t have access to an employer plan or want additional retirement savings options. Even small, consistent contributions can grow substantially over time thanks to compound interest.

If you’re over 50, take advantage of catch-up contributions that allow you to contribute more to retirement accounts than younger workers. These higher contribution limits can help accelerate your retirement savings if you’re feeling behind.

Building New Financial Goals and Dreams

While much of post-divorce financial planning focuses on recovery and stability, it’s equally important to look forward and establish new goals that excite and motivate you. This shift from survival mode to growth mode marks an important psychological transition in your financial journey.

Think about what you want your life to look like in five or ten years. Maybe you want to buy a new home, travel to places you’ve always dreamed of visiting, start a business, or help your children with college expenses. These goals give your financial planning purpose beyond just paying bills and staying afloat.

Break larger goals into smaller, manageable steps with specific timelines. If you want to buy a house in three years, calculate how much you need for a down payment and closing costs, then determine how much you need to save each month to reach that target.

Consider working with a financial advisor, especially if you received significant assets in the divorce or feel overwhelmed by investment decisions. A good advisor can help you develop a comprehensive financial plan that balances your immediate needs with your long-term goals.

Don’t forget to update your estate planning documents, including your will, beneficiary designations on retirement accounts and life insurance policies, and any powers of attorney. These changes are often overlooked but are crucial for protecting your financial interests and ensuring your wishes are carried out.

Moving Forward with Confidence

Rebuilding financial stability after divorce is undoubtedly challenging, but it’s also an opportunity to create the financial life you want on your own terms. Every step you take—from creating that first post-divorce budget to making your first retirement contribution as a single person—is an investment in your future independence and security.

Remember that progress isn’t always linear. You might have setbacks or months where you can’t save as much as you’d like, and that’s okay. What matters is maintaining forward momentum and staying committed to your financial well-being.

Be patient with yourself during this process. Financial recovery takes time, and comparing your progress to others or to your pre-divorce situation isn’t helpful. Focus on the positive changes you’re making and celebrate small victories along the way.

Most importantly, view this as a fresh start rather than a setback. Many people discover that managing their finances independently gives them a sense of empowerment and control they never experienced before. You have the opportunity to build a financial future that reflects your values, priorities, and dreams—and that’s something truly worth working toward.

Your journey to financial stability after divorce won’t happen overnight, but with patience, persistence, and the right strategies, you can create a secure and prosperous future. Take it one step at a time, stay focused on your goals, and remember that every day is a chance to make progress toward the financial independence you deserve.