How to Build a Secure Retirement Plan: Essential Insights for Your Financial Future

Picture this: you’re 65 years old, sitting on your porch with a cup of coffee, watching the sunrise without a care in the world about money. Sounds pretty good, right? But here’s the reality check – that peaceful retirement doesn’t happen by accident. It takes careful planning, smart decisions, and yes, starting earlier than you think you need to.

Building a secure retirement plan isn’t just about throwing money into a 401(k) and hoping for the best. It’s about creating a comprehensive strategy that’ll support the lifestyle you want when you’re ready to hang up your work boots. Whether you’re 25 and retirement feels like a distant dream, or 55 and suddenly realizing time is running short, this guide will walk you through the essential steps to build a retirement plan that actually works.

Understanding the Foundation of Retirement Planning

Before we dive into the nitty-gritty details, let’s talk about what retirement planning really means. At its core, it’s about replacing your current income when you stop working. Most financial experts suggest you’ll need about 70-80% of your pre-retirement income to maintain your standard of living. But here’s where it gets interesting – some people need more, some need less, depending on their plans.

Think about it this way: if you’re planning to travel the world, you might need more than someone who wants to stay home and tend their garden. If your mortgage will be paid off, you’ll need less than someone still making payments. The key is being honest about what you want your retirement to look like.

The traditional “three-legged stool” of retirement – Social Security, employer-sponsored plans, and personal savings – is still relevant, but it’s evolved. Social Security might cover basic expenses, but it’s probably not going to fund that dream vacation to Italy. Your employer’s 401(k) match is free money you absolutely shouldn’t leave on the table. And personal savings? That’s where you have the most control and potentially the biggest impact.

Starting Your Retirement Savings Journey

Here’s something that might surprise you: the most powerful tool in retirement planning isn’t picking the perfect investment or timing the market. It’s time itself. Thanks to compound interest, starting early can make a massive difference in your final nest egg.

Let’s say Sarah starts saving $200 a month at age 25, and her friend Mike starts saving $400 a month at age 35. Assuming a 7% annual return, by age 65, Sarah will have about $525,000, while Mike will have around $395,000. Sarah saved less money overall but ended up with more because she had those extra ten years of compound growth working for her.

But don’t panic if you’re getting a later start. The important thing is to begin now, wherever you are. Even if you can only save $50 a month initially, that’s $50 more than you were saving before. You can always increase your contributions as your income grows or your expenses decrease.

When you’re just starting out, focus on building the habit first. Set up automatic transfers to your retirement accounts so you’re paying yourself first. Many people find it easier to save money they never see in their checking account. Start with whatever amount feels manageable, then gradually increase it by 1% each year or whenever you get a raise.

Maximizing Employer-Sponsored Retirement Plans

If your employer offers a 401(k) or similar retirement plan, this should probably be your first stop. Why? Because it’s often the closest thing to free money you’ll ever find. Many employers offer matching contributions – essentially, they’ll add money to your account based on how much you contribute.

Here’s how it typically works: your employer might match 50% of your contributions up to 6% of your salary. So if you make $50,000 and contribute 6% ($3,000), your employer adds another $1,500. That’s an immediate 50% return on your investment, which is pretty hard to beat in any market.

The contribution limits for 401(k) plans are quite generous. For 2024, you can contribute up to $23,000 if you’re under 50, and $30,500 if you’re 50 or older thanks to catch-up contributions. These limits tend to increase with inflation, so they’ll likely be higher by the time you’re reading this.

One strategy that works well for many people is to increase their 401(k) contribution every time they get a raise. If you get a 3% salary increase, bump your retirement contribution by 1% and use the remaining 2% for current expenses. This way, you’re steadily increasing your savings rate without feeling a pinch in your monthly budget.

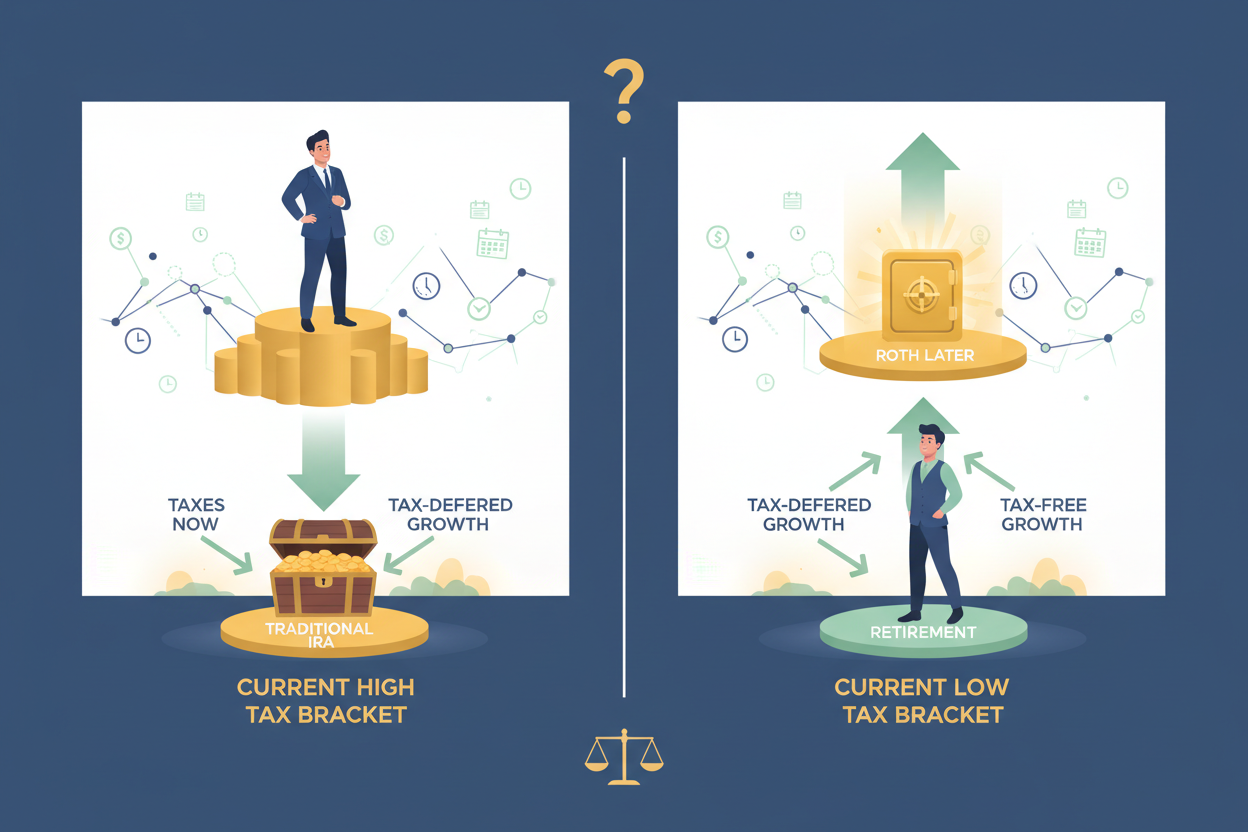

Exploring Individual Retirement Accounts

Individual Retirement Accounts, or IRAs, give you more control over your investment choices and can be excellent supplements to employer-sponsored plans. There are two main types: Traditional and Roth IRAs, and choosing between them is one of the most important decisions you’ll make.

With a Traditional IRA, you get a tax deduction now but pay taxes when you withdraw the money in retirement. A Roth IRA works the opposite way – you pay taxes on the money now, but withdrawals in retirement are tax-free. The contribution limit for 2024 is $7,000 for both types, with an additional $1,000 catch-up contribution if you’re 50 or older.

So which should you choose? It often comes down to your current tax bracket versus what you expect in retirement. If you’re in a high tax bracket now and expect to be in a lower one in retirement, a Traditional IRA might make sense. If you’re in a lower bracket now or expect to be in a higher one later, Roth could be the better choice.

Many financial advisors suggest having both types of accounts to give you tax flexibility in retirement. You can withdraw from whichever account makes the most sense tax-wise in any given year. This strategy, called tax diversification, can help you manage your tax burden throughout retirement.

Investment Strategies for Long-Term Growth

Once you’ve got your accounts set up, you need to decide how to invest the money. This is where many people get overwhelmed, but it doesn’t have to be complicated. The key principles are diversification, keeping costs low, and maintaining a long-term perspective.

Diversification means spreading your money across different types of investments – stocks, bonds, and perhaps some international investments. The exact mix depends on your age, risk tolerance, and time until retirement. A common rule of thumb is to subtract your age from 100 to determine what percentage should be in stocks. So if you’re 30, you might put 70% in stocks and 30% in bonds.

Target-date funds have become increasingly popular because they automatically adjust this mix as you get older. If you’re planning to retire in 2055, you’d choose a 2055 target-date fund, and it will gradually become more conservative as you approach retirement. These funds aren’t perfect for everyone, but they’re a solid choice if you want a hands-off approach.

Keep an eye on fees, as they can eat into your returns over time. A fund charging 1.5% annually versus one charging 0.5% might not seem like much, but over 30 years, that 1% difference could cost you tens of thousands of dollars. Look for low-cost index funds, which simply track market indexes rather than trying to beat them.

Planning for Healthcare Costs in Retirement

Here’s something that catches many retirees off guard: healthcare costs. Fidelity estimates that the average couple retiring at 65 will need about $300,000 to cover healthcare expenses throughout retirement. Medicare helps, but it doesn’t cover everything, and it certainly doesn’t cover long-term care.

If your employer offers a Health Savings Account (HSA), it can be one of the best retirement planning tools available. HSAs offer a triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. After age 65, you can withdraw money for any purpose (though you’ll pay taxes on non-medical withdrawals).

For 2024, you can contribute up to $4,150 to an HSA if you have individual coverage, or $8,300 for family coverage. If you’re 55 or older, you can add an extra $1,000 as a catch-up contribution. The key is to think of your HSA as a retirement account rather than just a way to pay current medical bills.

Long-term care insurance is another consideration. The odds of needing some form of long-term care are higher than many people realize – about 70% according to the Department of Health and Human Services. Long-term care insurance can be expensive, but it’s generally cheaper when you buy it younger and healthier.

Social Security Optimization Strategies

Social Security will likely be part of your retirement income, but maximizing your benefits requires some strategic thinking. Your benefit amount depends on your earnings history and when you choose to start receiving payments. You can start as early as 62, but your benefits will be reduced. Wait until your full retirement age (66-67 depending on when you were born), and you’ll get your full benefit. Wait until 70, and you’ll get delayed retirement credits that increase your benefit by about 8% per year.

For many people, delaying Social Security makes financial sense if they can afford to wait. Let’s say your full retirement age benefit would be $2,000 per month. If you start at 62, you might only get $1,400. But if you wait until 70, you could get about $2,640. That’s a significant difference that continues for the rest of your life.

If you’re married, the decision becomes more complex because you need to consider spousal benefits and survivor benefits. The higher-earning spouse might want to delay claiming to maximize the survivor benefit, while the lower-earning spouse might claim earlier. These decisions can have major long-term financial implications, so it’s often worth consulting with a financial advisor.

Creating Multiple Income Streams

Relying solely on traditional retirement accounts might not be enough, especially if you want financial flexibility. Creating multiple income streams can provide security and potentially allow you to retire earlier or more comfortably.

Real estate can be one option, whether through rental properties or Real Estate Investment Trusts (REITs) if you don’t want to deal with being a landlord. Dividend-paying stocks can provide regular income, though dividends aren’t guaranteed. Some people build side businesses that can continue generating income in retirement.

The key is to start building these alternative income streams while you’re still working. It takes time to build a profitable rental property portfolio or grow a side business to meaningful levels. Plus, having multiple income sources can provide a buffer if one source has problems.

Don’t overlook the value of reducing expenses, which is essentially the same as creating income. Paying off your mortgage before retirement eliminates a major monthly expense. Downsizing your home can reduce both your mortgage and ongoing maintenance costs. These strategies can significantly reduce how much you need to save for retirement.

Regular Review and Adjustment of Your Plan

Your retirement plan isn’t something you set up once and forget about. Life changes, markets fluctuate, and your goals might evolve. That’s why it’s important to review your plan regularly – at least annually, and whenever you have major life changes like marriage, divorce, job changes, or health issues.

During these reviews, look at whether you’re on track to meet your goals. Are you saving enough? Do your investments still make sense for your timeline and risk tolerance? Have your retirement goals changed? Maybe you’ve decided you want to retire earlier, or perhaps you’ve realized you’d like to work part-time longer than you originally planned.

Don’t be afraid to make adjustments. If you’re behind on your savings goals, you might need to save more, work a few years longer, or adjust your retirement lifestyle expectations. If you’re ahead of schedule, you might be able to take a bit more risk for potentially higher returns, or simply enjoy the peace of mind that comes with being well-prepared.

Market downturns can be particularly challenging psychologically, but they’re a normal part of investing. The key is to stay focused on your long-term goals and not make emotional decisions. In fact, market downturns can be opportunities to buy investments at lower prices, especially if you’re still years away from retirement.

Securing Your Financial Future

Building a secure retirement plan doesn’t happen overnight, and it’s not about making perfect decisions every time. It’s about making consistent, informed decisions over many years and adjusting course when needed. The most important step is starting, regardless of where you are in your career or how much you can initially save.

Remember that retirement planning is deeply personal. What works for your neighbor or coworker might not be the best strategy for you. Your plan should reflect your goals, risk tolerance, timeline, and financial situation. Don’t be afraid to seek help from qualified financial professionals, especially for complex decisions around Social Security, tax planning, or investment allocation.

The retirement landscape continues to evolve, with people living longer, healthcare costs rising, and traditional pensions becoming less common. But with proper planning, you can build a retirement that provides both financial security and the freedom to enjoy the fruits of your labor. Start today, stay consistent, and adjust as needed. Your future self will thank you for the effort you put in now.