Divorce Financial Planning: Steps for a Secure Future

Going through a divorce is never easy, and while emotions run high, one of the most critical aspects you’ll need to address is your financial future. The decisions you make during this challenging time can impact your financial well-being for years to come. Whether you’re just beginning to consider divorce or you’re already in the middle of proceedings, having a solid financial plan is essential for rebuilding your life on stable ground.

Divorce financial planning isn’t just about dividing assets—it’s about understanding your complete financial picture, protecting your interests, and setting yourself up for long-term success. The process might feel overwhelming, especially when you’re dealing with emotional stress, but taking it step by step can help you navigate this transition with confidence and clarity.

Understanding Your Current Financial Situation

Before you can plan for your financial future, you need to have a crystal-clear picture of where you stand today. This means gathering every piece of financial information you can find, even if it feels tedious or overwhelming. Think of this as building the foundation for your new financial life—the stronger this foundation, the more secure your future will be.

Start by collecting bank statements, investment account records, retirement account statements, insurance policies, tax returns from the past three to five years, and documentation of all debts including credit cards, mortgages, and loans. Don’t forget about less obvious assets like business interests, stock options, or valuable personal property. If your spouse has been the primary financial manager in your relationship, this process might reveal information you weren’t fully aware of before.

Creating a comprehensive net worth statement will give you a clear snapshot of your marital assets and liabilities. This document becomes crucial during divorce negotiations and helps you understand what’s at stake. Remember, in many states, assets acquired during marriage are considered marital property, regardless of whose name is on the account.

Assembling Your Financial Team

Divorce financial planning is complex enough that you shouldn’t try to handle it alone. Building a team of qualified professionals can make the difference between a financial outcome that sets you back and one that positions you for future success. Your team should include several key players, each bringing specialized expertise to your situation.

A divorce attorney who understands the financial complexities of your case is essential. Look for someone who has experience with cases similar to yours, especially if you have significant assets, own a business, or have complex retirement accounts. Your attorney will help protect your legal rights and ensure that any financial agreements are fair and enforceable.

A Certified Divorce Financial Analyst (CDFA) can be invaluable in helping you understand the long-term implications of different settlement scenarios. These professionals specialize in the financial aspects of divorce and can run projections showing how different asset division arrangements might affect your future financial security. They can also help you understand the tax implications of various settlement options.

Don’t overlook the importance of a good accountant, especially if you have complex tax situations, own a business, or need help understanding the tax consequences of asset division. A financial advisor can help you develop a post-divorce investment strategy and retirement planning approach that aligns with your new circumstances.

Protecting Your Assets During Proceedings

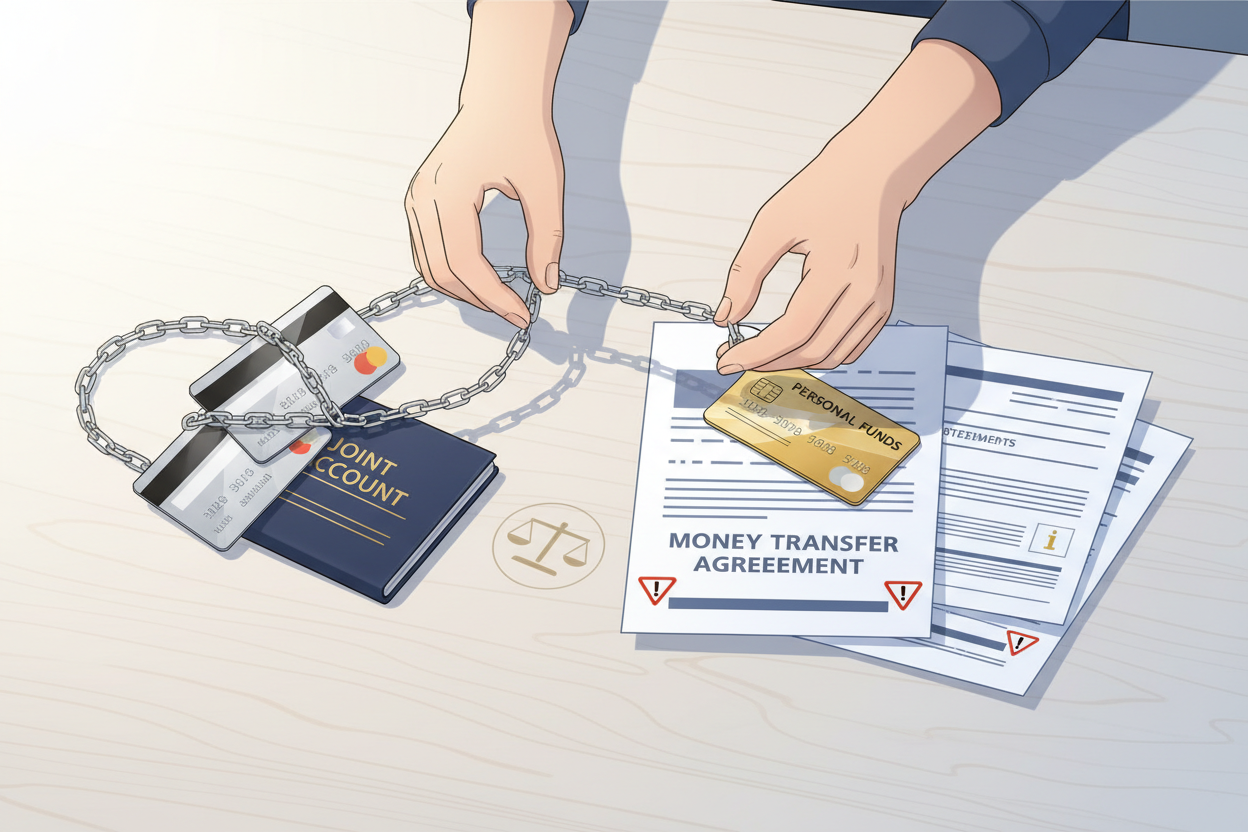

Once divorce proceedings begin, protecting your assets becomes a priority. This doesn’t mean hiding money or being dishonest—quite the opposite. Transparency and proper documentation are your best protection against accusations of financial misconduct. However, there are legitimate steps you can take to safeguard your financial interests during this vulnerable time.

Opening individual bank accounts and credit cards in your name alone is often one of the first steps. This ensures you have access to funds for living expenses and legal fees, and it begins the process of establishing your independent credit history. However, be careful about how you fund these accounts—transferring large amounts from joint accounts without agreement or court approval could be viewed unfavorably.

Monitor all joint accounts and credit cards closely. Set up alerts for transactions so you’re immediately aware of any activity. If you’re concerned about unauthorized spending, you might need to seek court intervention to freeze accounts or establish spending limits. Document everything—keep records of all financial transactions, communications about money, and changes to account ownership or beneficiaries.

Review and update beneficiaries on all accounts where appropriate, but be aware that some states have automatic restraining orders that prevent changes to insurance beneficiaries or retirement account designations during divorce proceedings. Check with your attorney before making any changes.

Creating a Post-Divorce Budget

One of the most sobering aspects of divorce financial planning is realizing that the same income that supported one household will now need to support two. This reality makes budgeting absolutely critical for your financial survival and future success. Your post-divorce budget needs to be both realistic about your new circumstances and strategic about your long-term goals.

Start by calculating your expected post-divorce income, including salary, any spousal support you might receive, child support, and investment income. Be conservative in your estimates—it’s better to be pleasantly surprised than to fall short of your projections. Then, list all your expected expenses, starting with fixed costs like housing, insurance, and loan payments, then moving to variable expenses like groceries, utilities, and discretionary spending.

Housing often represents the biggest budget challenge in divorce. The family home might no longer be affordable on a single income, even if you receive it in the settlement. Consider all costs of homeownership, including maintenance, repairs, property taxes, and insurance. Sometimes, selling the home and splitting the proceeds provides more financial flexibility than keeping a house you can’t afford.

Don’t forget to budget for new expenses that come with being single again. You might need to pay for services your spouse previously handled, like lawn care or home repairs. You’ll also need to consider the cost of establishing new insurance policies, potentially higher individual health insurance premiums, and the ongoing costs of legal and financial advice.

Retirement and Long-Term Financial Security

Divorce can significantly impact your retirement timeline and strategy, especially if you’re divorcing later in life or if retirement accounts represent a substantial portion of your marital assets. Understanding how to protect and rebuild your retirement security is crucial for your long-term financial well-being.

If you’re entitled to a portion of your spouse’s retirement accounts, make sure you understand the different types of accounts and their tax implications. Traditional 401(k) and IRA accounts will be taxed when you withdraw the money, while Roth accounts provide tax-free withdrawals in retirement. The timing and method of dividing these accounts can have significant tax consequences, so professional guidance is essential.

A Qualified Domestic Relations Order (QDRO) is often required to divide employer-sponsored retirement plans like 401(k)s without triggering penalties or taxes. This legal document must be carefully prepared and approved by the plan administrator. Mistakes in QDRO preparation can be costly and difficult to correct, so working with experienced professionals is worth the investment.

Consider how the divorce affects your Social Security benefits. If you were married for at least 10 years, you might be entitled to benefits based on your ex-spouse’s earnings record, which could be higher than benefits based on your own earnings. These divorced spouse benefits don’t reduce your ex-spouse’s benefits, and you can claim them even if your ex-spouse remarries.

Reassess your retirement timeline and savings strategy based on your new circumstances. You might need to work longer than originally planned, increase your savings rate, or adjust your retirement lifestyle expectations. The sooner you face these realities and adjust your strategy accordingly, the better positioned you’ll be for a secure retirement.

Insurance and Estate Planning Updates

Divorce necessitates a complete review and overhaul of your insurance coverage and estate planning documents. These updates are not just administrative tasks—they’re critical steps in protecting your financial security and ensuring your wishes are properly documented and legally enforceable.

Health insurance is often the most immediate concern, especially if you’ve been covered under your spouse’s employer plan. You’ll need to understand your options, which might include COBRA coverage, purchasing an individual policy through the health insurance marketplace, or obtaining coverage through your own employer. Factor the cost of health insurance into your budget planning, as individual coverage is typically more expensive than family coverage.

Life insurance needs careful attention during and after divorce. If you have children together, you might want to maintain life insurance with your ex-spouse as beneficiary to ensure child support obligations can be met if something happens to you. Conversely, you might require your ex-spouse to maintain life insurance to protect alimony or child support payments. The divorce decree should specify these requirements clearly.

Update all your estate planning documents, including your will, power of attorney, healthcare directive, and any trust documents. Remove your ex-spouse as beneficiary and decision-maker unless you specifically want them to retain these roles. Name new beneficiaries for all accounts and policies, and consider naming contingent beneficiaries as well.

Tax Considerations and Strategies

Divorce brings numerous tax implications that can significantly impact your financial outcome if not properly managed. Understanding these tax consequences and planning accordingly can save you thousands of dollars and help you make more informed decisions during settlement negotiations.

The timing of your divorce can affect your tax filing status and available deductions. If your divorce is finalized by December 31st, you’ll need to file as single or head of household for that entire tax year. Sometimes, it might be beneficial to delay finalizing the divorce until after the new year, depending on your specific tax situation.

Alimony payments have specific tax rules that changed significantly with the Tax Cuts and Jobs Act. For divorces finalized after December 31, 2018, alimony payments are no longer deductible by the payer or taxable income to the recipient. This change affects the economics of alimony negotiations and might influence whether you prefer to receive more alimony or more assets in your settlement.

Asset transfers between spouses during divorce are generally not taxable events, but the tax basis of transferred assets carries over to the recipient. This means you could inherit a significant tax liability with certain assets. For example, if you receive stock that your spouse purchased years ago at a much lower price, you’ll owe capital gains tax on the appreciation when you eventually sell it.

Building Your Independent Financial Future

Once the divorce is finalized, your focus shifts from protection and negotiation to building and growing your independent financial life. This phase is about taking control of your financial destiny and creating the security and prosperity you want for your future.

Establishing and building your individual credit history becomes important, especially if most accounts were in your spouse’s name during marriage. Keep credit cards that were in your name, and consider becoming an authorized user on accounts belonging to family members with good credit. Pay all bills on time, keep credit utilization low, and monitor your credit report regularly for errors or fraudulent activity.

Develop an investment strategy that aligns with your new goals, risk tolerance, and timeline. Your investment approach might need to be more conservative if you’re closer to retirement or if you have less time to recover from market downturns. Consider working with a fee-only financial advisor who can help you develop a comprehensive financial plan for your new circumstances.

Focus on rebuilding your emergency fund, which should cover three to six months of living expenses. Having this financial cushion provides peace of mind and protects you from having to rely on credit cards or loans for unexpected expenses. Start small if necessary—even saving $25 per month is progress toward this goal.

Consider new opportunities for income growth, whether through career advancement, additional education, starting a side business, or developing new skills. Divorce often provides an opportunity to reassess your career goals and make changes that might not have been possible during marriage.

Divorce financial planning is undoubtedly challenging, but it’s also an opportunity to take control of your financial life in ways you might never have experienced before. By approaching the process systematically, seeking professional guidance when needed, and staying focused on your long-term goals, you can emerge from divorce with a solid foundation for financial security and independence. Remember that rebuilding takes time, and be patient with yourself as you navigate this significant life transition. Your future financial success depends on the decisions and actions you take today, so invest the time and effort needed to get them right.